Vietnam and Thailand compete for ASEAN investment, but the EU’s carbon border rules are reshaping the balance. (Photo: iStock)

In January 2026, the EU’s Carbon Border Adjustment Mechanism (CBAM), comes into force, turning carbon emissions into a decisive factor in export pricing and market competitiveness. For Southeast Asia’s manufacturing sector, the policy currently targets carbon intensive industries such as steel, cement and aluminum, but its effects are already rippling through supply chains.

Vietnam has seen rapid growth in exports to the European market in recent years, while Thailand retains a more mature manufacturing base and industrial ecosystem. As carbon costs begin to reshape trade rules, the foundations of manufacturing competitiveness are shifting. Against this backdrop, Vietnam and Thailand are emerging as key rivals in attracting investment across ASEAN. As the EU’s CBAM quietly raises the bar for market access, the question is no longer whether competition will intensify, but which country is better positioned to win in an increasingly carbon constrained world.

Export structures and CBAM exposure in Thailand and Vietnam

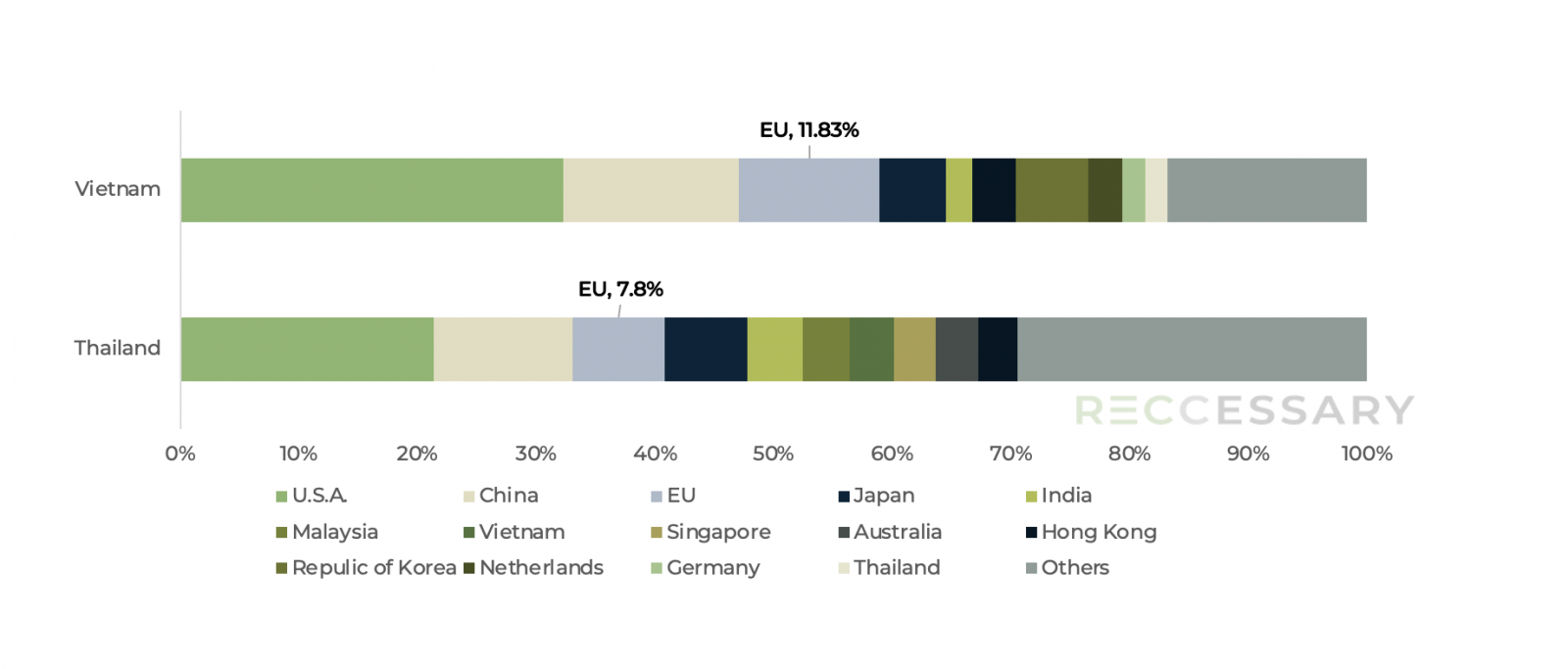

From an export structure perspective, Vietnam relies more heavily on the European market than Thailand. Latest trade data show that the EU is the third largest export destination for both countries, but the share is significantly higher for Vietnam. In 2025, exports to the EU accounted for about 11.83% of Vietnam’s total exports, compared with roughly 7.8% for Thailand. As carbon costs begin to factor into trade, Vietnam’s manufacturing sector will come under more immediate pressure than Thailand’s.

Figure 1. Top 10 export destinations for Thailand and Vietnam in 2025 [1]

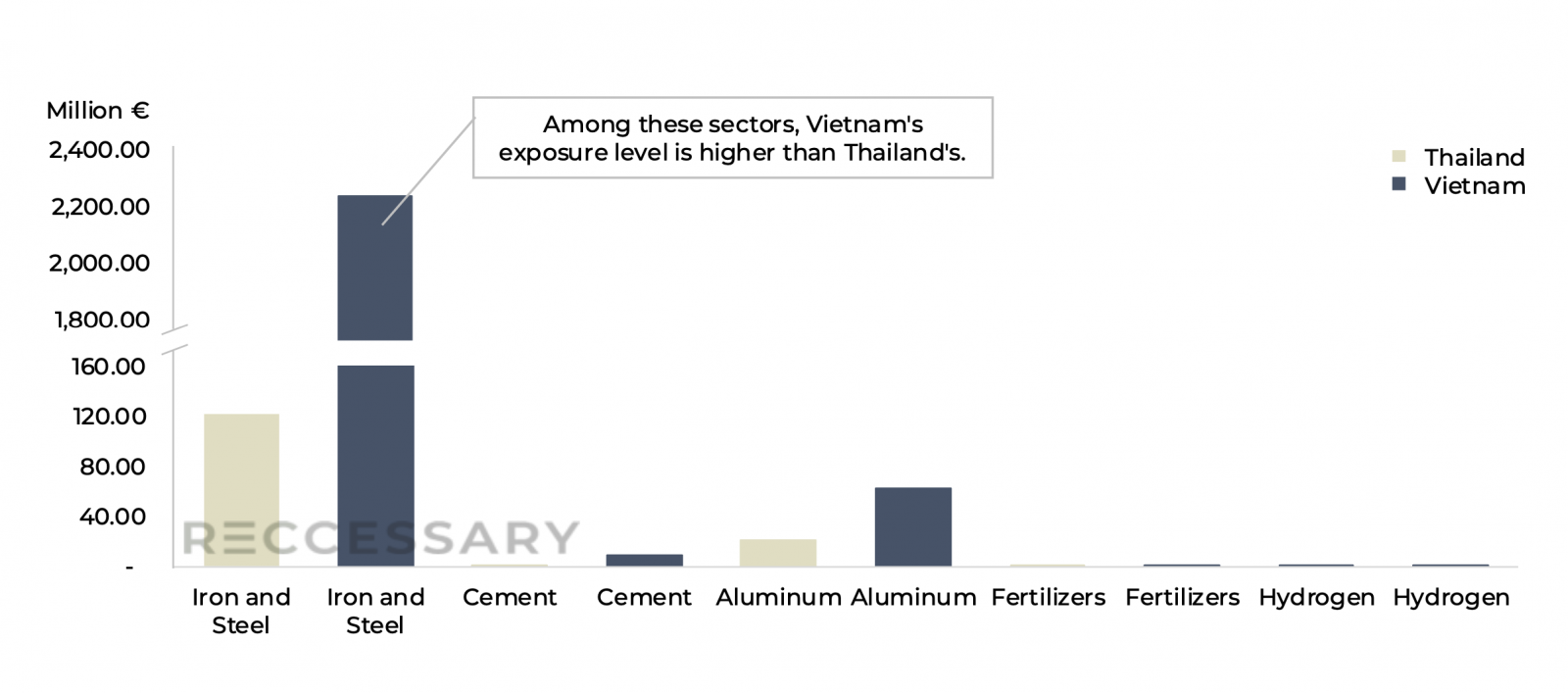

Looking specifically at the carbon intensive sectors covered in CBAM’s initial phase, the gap between Vietnam and Thailand becomes much more pronounced. Steel, cement and aluminum are among the first industries targeted, and Vietnam’s exports to the EU in these sectors far exceed Thailand’s, especially in steel. In 2024, Vietnam exported more than EUR 2.2 billion worth of steel products to the EU, over 18 times Thailand’s level.

The difference is also evident in export composition. CBAM covered sectors made up about 4.2% of Vietnam’s EU bound exports in 2024, compared with just 0.5% for Thailand. While both countries face the same tightening carbon rules, Vietnam’s large scale steel exports leave a significant share of its output directly exposed to carbon tariffs. As a result, when CBAM begins full pricing in 2027, Vietnam will face more urgent decarbonization pressure than Thailand.

Figure 2. Exports of CBAM covered products to the EU from Thailand and Vietnam [2]

Financial impact under the EU’s default value mechanism

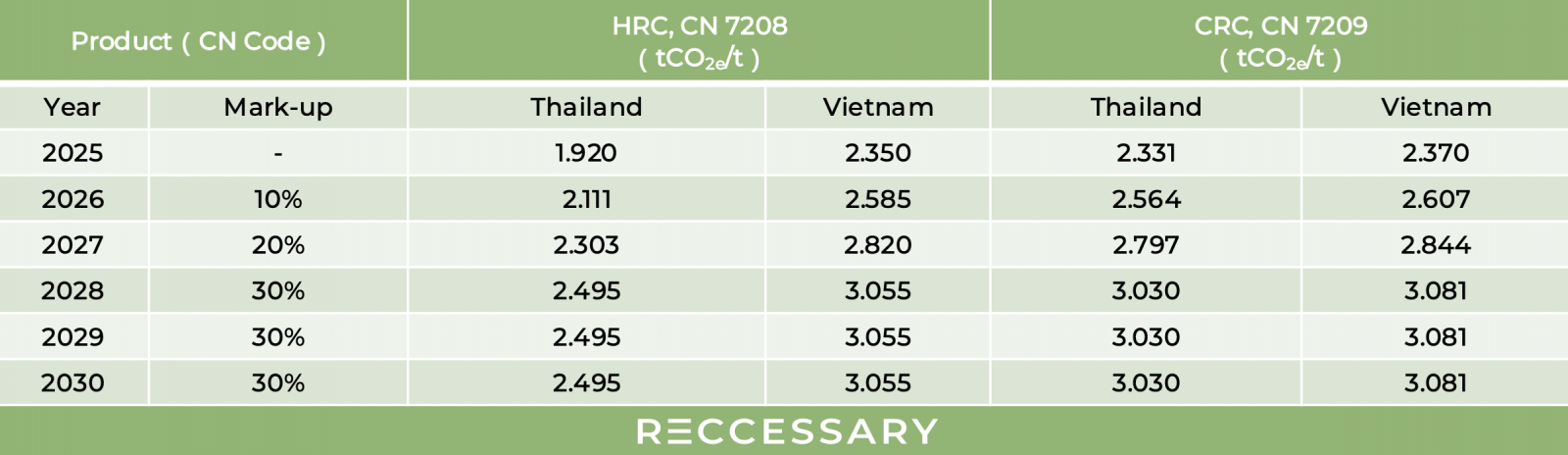

Beyond overall export exposure, CBAM’s impact on corporate competitiveness is set to intensify at the reporting stage. Under the EU’s implementing regulation (EU) 2025/2621, issued in December 2025, companies that fail to provide verified emissions data must apply default values set by the EU. To encourage accurate disclosure, the regulation introduces a tiered mark-up mechanism, set at 10% in 2026, rising to 20% in 2027 and reaching 30% from 2028 onward.

To illustrate the cost implications of default values, the following analysis focuses on two key steel products, hot rolled coil (HRC, CN 7208) and cold rolled coil (CRC, CN 7209). [3]

Table 1. EU CBAM default values for Thailand and Vietnam [4]

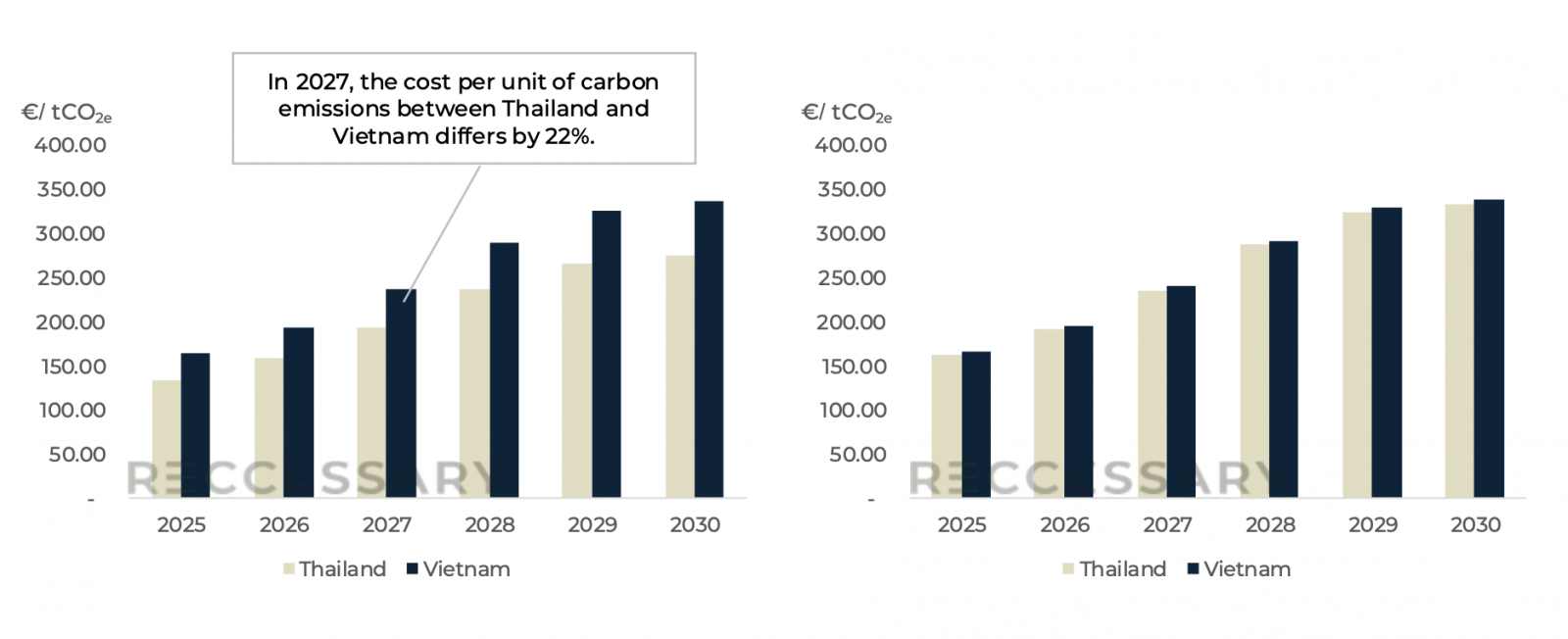

Taking 2027 as an example, when a 20% mark-up on default values is applied, hot rolled coil shows the most pronounced competitiveness gap. Vietnam’s carbon cost reaches around EUR 238 per tonne, compared with about EUR 194 for Thailand, resulting in a unit cost difference of roughly 22% for the same product.

For a typical EU bound order of 10,000 tonnes, this gap becomes material. Under a scenario of rising default values and carbon prices, Vietnamese producers would face an additional carbon cost of about EUR 436,000 compared with their Thai counterparts. This added burden could erode margins in bulk steel trades and, in some cases, lead to the loss of orders.

By contrast, the gap narrows significantly further down the value chain. For cold rolled coil, the difference in carbon costs between Thailand and Vietnam is only around 1.67% in 2027. A similar pattern can be observed across other stages of the supply chain, including upstream semi-finished iron or non-alloy products (CN 72071210) and downstream processes such as hot dip galvanizing (HDG, CN 7210).

This suggests that as production shifts from upstream heat intensive processes to downstream electricity intensive ones, carbon costs become increasingly dependent on the level of power sector decarbonization.

Figure 3 (left). CBAM carbon cost impact assessment for HRC (CN 7208)

Figure 4 (right). CBAM carbon cost impact assessment for CRC (CN 7209)

Differences in the maturity of decarbonization frameworks

A closer look at carbon pricing developments in Thailand and Vietnam shows that the two countries are taking markedly different approaches to responding to the pressures posed by the EU’s CBAM.

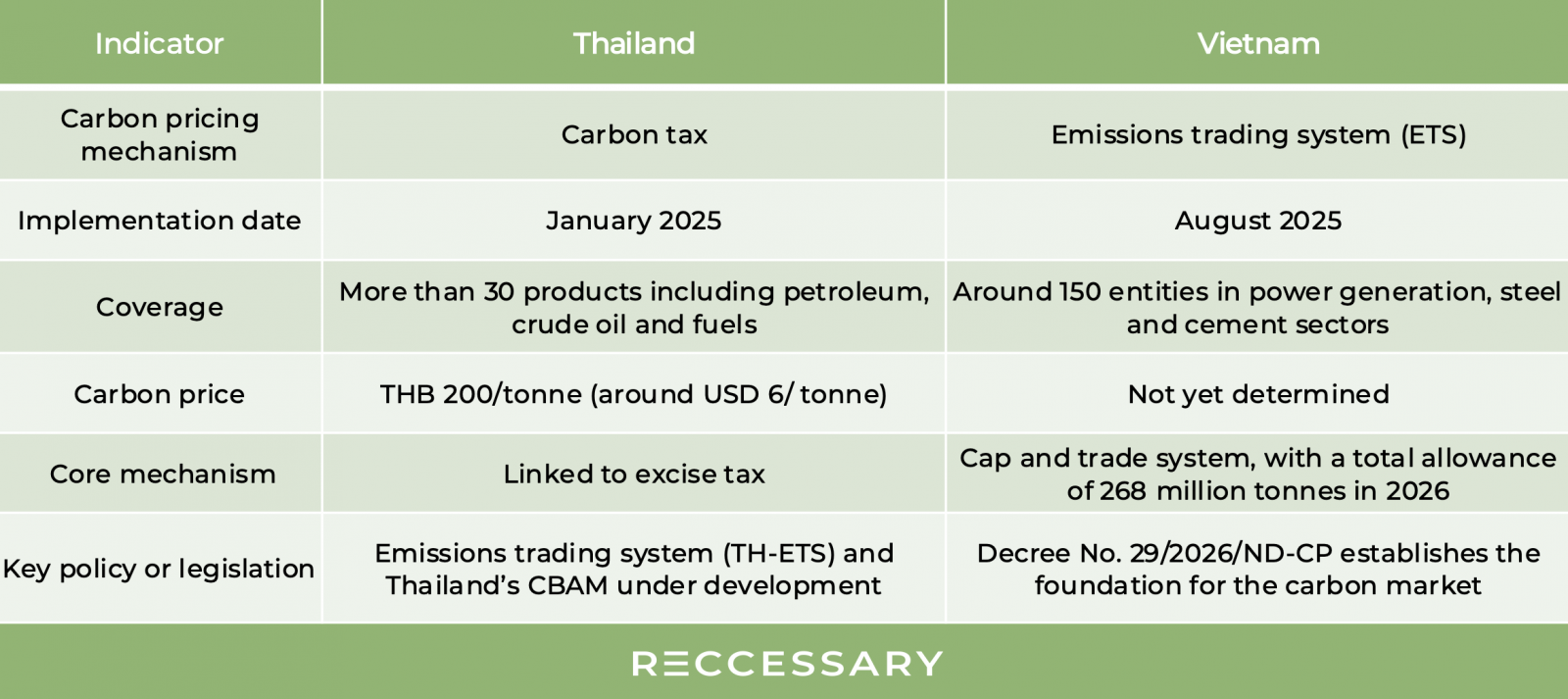

Table 2. Comparison of carbon pricing systems in Thailand and Vietnam

Based on currently announced policies, Thailand formally introduced a carbon tax in January 2025, covering more than 30 products including petroleum, crude oil and fuels, at a rate of THB 200 per tonne (around USD 6). The tax is implemented through linkage with the existing excise tax system. At the same time, the Thai government has outlined plans to develop an emissions trading system (TH-ETS) and a domestic CBAM, signaling a gradual move toward alignment with the EU framework.

Vietnam, by contrast, has adopted an emissions trading system (V-ETS) centered on a cap-and-trade approach. Under Decree No. 29/2026/ND-CP, the system came into effect in August 2025, initially covering around 150 companies (about 110 facilities) in sectors such as power generation, steel and cement, with a total emissions cap of 268 million tonnes set for 2026. While the carbon price has yet to be determined, the design of the system aligns closely with the EU ETS, underscoring Vietnam’s push to accelerate the development of its carbon market.

As CBAM takes shape, Thailand appears better prepared, with a more established policy framework that gives it a short-term advantage. Vietnam, meanwhile, is moving quickly on policy, but still needs to strengthen execution at the corporate level.

Thailand leads in experience, while Vietnam moves fast on policy

Taken together, these three dimensions show that the EU’s CBAM is redefining the foundations of manufacturing competitiveness. Thailand, supported by earlier carbon management experience and greater policy stability, currently holds stronger risk management capacity, allowing it to maintain relatively stable export competitiveness in the initial phase of CBAM. Vietnam, by contrast, faces greater exposure due to its export structure and industrial scale. While policy momentum is strong, gaps in corporate level implementation may still translate into rising cost pressures in the near term.

This gap, however, is unlikely to remain fixed. As Vietnam accelerates the development of its ETS and power market reforms, it could still reverse the trajectory over time, particularly if it strengthens its MRV framework and expands low carbon power supply. Conversely, if Thailand fails to further enhance its policy framework, its current advantage may gradually erode.

Ultimately, the outcome will depend on which country can more quickly build a comprehensive carbon management system and reduce reliance on default values. Those that do will be better positioned to compete under the EU’s evolving carbon-based trade regime.

Notes

[1] Source: Vietnam Customs; Thailand Ministry of Commerce

[2] Source: Eurostat; product classification based on SITC codes

[3] Based on a carbon price of EUR 75/tonne in 2026, with annual increases

[4] Source: Commission Implementing Regulation (EU) 2025/2621