(1).jpg)

Nature-related management is following a similar trajectory to carbon management.(Image:Pixabay)

On Oct. 6, 2025, the International Organization for Standardization (ISO) released ISO 17298:2025, marking its first international standard focused on biodiversity. Unlike the policy-oriented Kunming–Montreal Global Biodiversity Framework (GBF) and the disclosure-driven Taskforce on Nature-related Financial Disclosures (TNFD), ISO 17298:2025 is designed for implementation. It aims to support companies in integrating biodiversity into governance, risk management, and business operations.

This development mirrors the evolution of carbon management. Companies typically begin with target setting and disclosure, followed by emissions measurement to understand their footprint. This then enables the identification of hotspots, the implementation of reduction strategies, and ultimately the transition toward carbon neutrality.

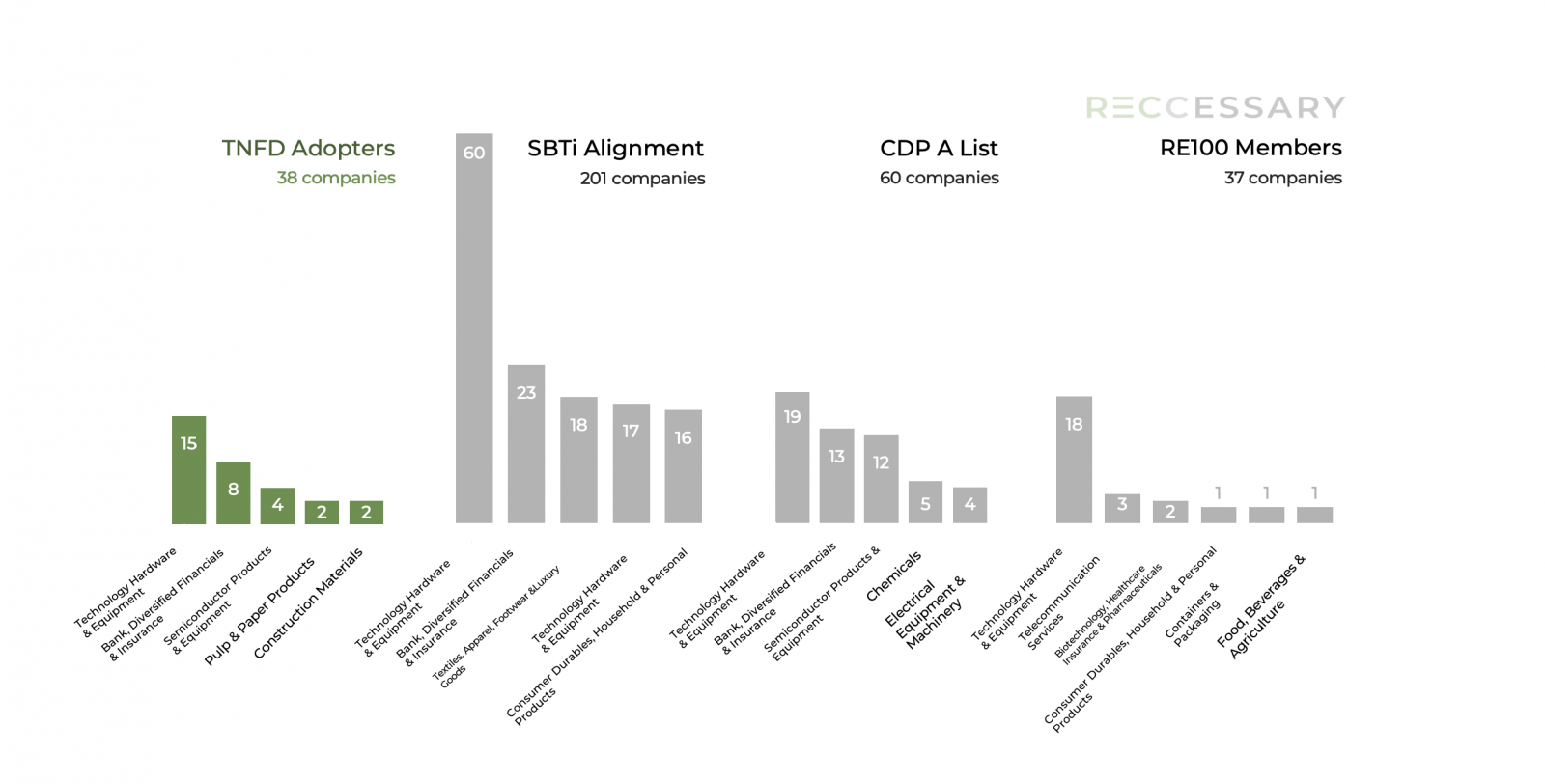

Figure 1. Adoption of major sustainability frameworks across industries in Taiwan[1]

The evolution of nature-related frameworks is increasingly mirroring the development path of carbon management. Taking the TNFD as an example, although its adoption in Taiwan remains lower than carbon-focused initiatives such as the Science Based Targets initiative (SBTi) and climate disclosure platforms like CDP, the number of participating companies has reached a meaningful scale. This suggests that businesses are beginning to take nature-related disclosure more seriously.

ISO 17298:2025 is designed to complement existing frameworks such as ISO 14001 (environmental management) and other nature-related standards. Looking ahead, more companies are expected to leverage these tools to strengthen implementation at the operational level, enabling them to better respond to future disclosure and compliance requirements.

Unlock the full article to explore three key takeaways:

- Three sectors, raw materials, energy, and food and beverages, account for the largest share of biodiversity impacts among listed companies in Taiwan, placing them in a high-risk category.

- Following the initial adoption of IFRS S1 and S2, most companies will have just two to three years to align with emerging nature-related disclosure standards.

- Within high-impact sectors, the majority of companies in industries such as chemicals, food, and steel have paid-in capital below TWD 5 billion, making implementation more challenging given limited resources.