.jpg)

Experts say policy frameworks in Vietnam and Thailand are outpacing execution capacity, giving early movers a competitive edge. (Photo: RECCESSARY)

Manufacturing competitiveness in Southeast Asia is shifting. For companies exporting to Europe, a carbon price is now embedded in every shipment of steel, aluminum, or cement. As enforcement approaches full implementation, the gap between factories with verified emissions data and those without will become increasingly difficult to close without timely action.

RECCESSARY’s webinar, “Beyond ASEAN: Mastering Decarbonization Strategy in Thailand and Vietnam,” held on April 21, brought together legal advisors, renewable energy developers, carbon market analysts, and corporate sustainability practitioners to assess the implications for site selection, energy procurement, and compliance planning.

The discussion converged on a clear diagnosis that policy frameworks in Vietnam and Thailand have advanced faster than on-the-ground execution capacity, and that companies treating carbon and clean energy as integrated investment decisions will hold a measurable edge by 2030.

RECCESSARY’s webinar, “Beyond ASEAN: Mastering Decarbonization Strategy in Thailand and Vietnam,” brought together legal, renewable energy, carbon market, and corporate sustainability experts. (Photo: RECCESSARY)

Steel’s carbon exposure is already repricing competitiveness

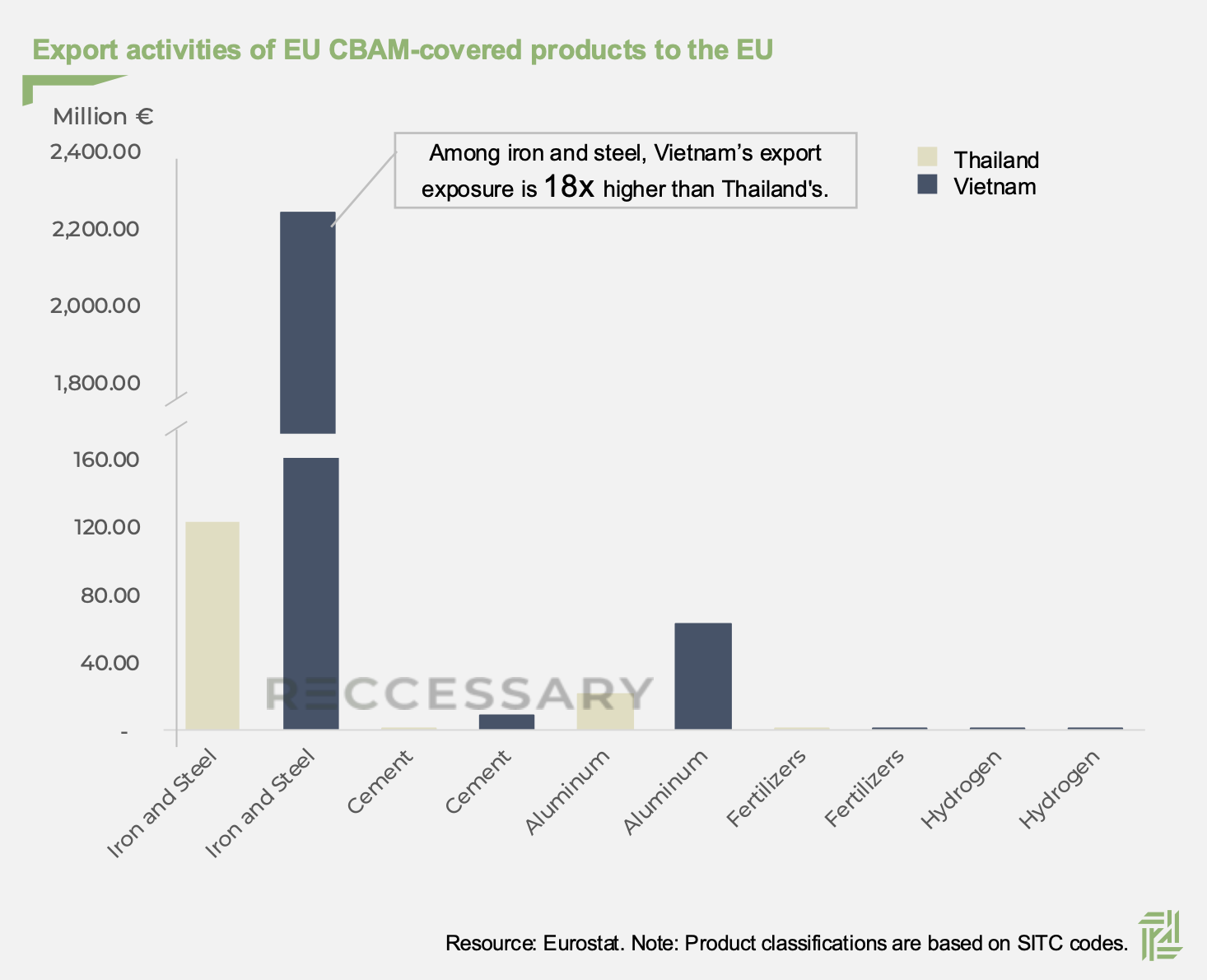

The impact of CBAM is most visible in Vietnam’s iron and steel sector, where exposure is concentrated and the cost of inaction is already measurable. In 2024, Vietnam’s iron and steel exports to the EU exceeded EUR 2.2 billion, compared with about EUR 120 million for Thailand, an exposure ratio of more than 18 to one for a single product category, according to Sherry Hu, carbon market analyst at RECCESSARY.

Vietnam’s push into blast furnace-based steelmaking sits at the center of this exposure. Hu noted that the country deliberately expanded integrated steel production capacity, covering the full process from raw materials to finished products, to move up the value chain and access export markets. “CBAM places a cost directly on that strategy. The more carbon-intensive the production route, the greater the penalty,” Hu said.

In 2024, Vietnam’s iron and steel exports to the EU far exceeded Thailand’s, with an exposure gap of more than 18 to one for a single product category. (Figure: RECCESSARY)

The urgency comes from the default value mechanism under EU Regulation 2025/2621. Facilities without verified, site-level emissions data must use country-level default values with added penalties of 10% in 2026, 20% in 2027, and 30% from 2028.

Hu’s analysis of hot-rolled coil (HRC) shows that by 2030, a Vietnamese producer relying on defaults would face carbon costs of EUR 336 per tonne, compared with EUR 274 for a Thai counterpart. This 22% gap reflects data transparency rather than actual emissions performance. For a 10,000-tonne shipment, that could mean up to EUR 616,000 in additional margin loss. “Data transparency has become a cost competitiveness issue,” Hu said.

Buyer behavior is already shifting. EU importers, who are responsible for CBAM certificate costs, have a direct incentive to source from suppliers with verified emissions data, since it lowers their compliance costs. Suppliers without such data become more expensive due to regulatory costs.

Differences between Vietnam and Thailand also reflect their carbon pricing systems. Thailand entered 2025 with a carbon tax and an integrated MRV system. Hu noted that over the next two to three years, this provides a more stable compliance environment, giving exporters a clearer framework to generate primary data, claim deductions, and meet EU customs requirements.

Vietnam’s ETS, launched in August 2025 and covering about 110 facilities across the power, steel, and cement sectors, points to stronger long-term ambition. Hu described Vietnam as being in a “dynamic transition,” where the regulatory architecture is in place but enterprise-level execution has yet to catch up.

In the longer term, carbon credit issuance in both countries remains heavily concentrated in renewable energy projects. Additionality constraints may limit the supply of high-quality credits as compliance demand increases, reducing the extent to which domestic carbon markets can offset CBAM liabilities, according to James Chen, carbon market research assistant at RECCESSARY.

DPPA frameworks open new pathways, but execution risks remain

For manufacturers seeking to reduce the carbon intensity of their electricity supply, Vietnam’s new DPPA framework marks a structural shift in renewable power procurement. Resolution 253, which took effect in March 2026, further expands eligibility to electricity retailers in industrial parks and economic zones, allowing demand aggregation at the zone level for the first time.

However, the gap between regulatory design and commercial execution remains significant, said VSE Lawyers’ managing partner Pham Mihn Hoang, who has advised on several early DPPA transactions. He pointed to three structural barriers consistently emerging as projects approach financial close. Grid curtailment without compensation creates revenue uncertainty, Contract for Difference (CfD) revenues tied to volatile spot prices raise financing risk, and overlapping tariff charges result in double payment, weakening the case for switching from standard retail tariffs.

Thailand’s 2 GW DPPA pilot, targeted for launch in 2026, is initially restricted to BOI-approved data centers with a minimum IT base load of 50 MW and allocates grid capacity on a first-come, first-served basis.

The permitting and approval process adds further pressure. From document preparation through construction, a typical project timeline runs close to 18 months. Developers without established local relationships and pre-identified land are likely to struggle to move quickly once the pilot opens, said Oscar Loza, Vietnam Country Manager and Regional Head of Business Development at Constant Energy.

Constant Energy has operated more than 93 MW of contracted rooftop solar in Thailand since 2017 and has pre-screened over 100 potential DPPA sites ahead of the pilot launch. (Photo: Constant Energy)

Closing the CBAM gap through carbon removal and verified data infrastructure

For manufacturers facing hard-to-abate Scope 1 and Scope 2 emissions that cannot be fully addressed through renewable electricity procurement alone, carbon dioxide removal is emerging as a practical transitional tool.

Biochar accounted for 87.6% of physical durable carbon removal delivered globally in 2024, making it the most deployable near-term option while other technologies continue to scale, according to Lisa Wu, manager of the carbon dioxide removal department at GreenJump Sustainability.

For ASEAN manufacturers, the most immediate entry point is partial material substitution, including replacing carbon-intensive inputs such as carbon black, a fossil-derived material widely used in rubber and plastics production, with biochar alternatives. Wu noted that even a 10 to 15% substitution can deliver measurable reductions in product carbon footprint, with direct implications for compliance costs and export competitiveness.

GreenJump is developing biochar projects aligned with Vietnam’s carbon trading framework, which allows eligible projects to sell up to 90% of credits internationally. (Screenshot from webinar)

Looking ahead, the next phase will hinge on how quickly companies translate awareness into concrete action. Many facilities hold emissions data but have not converted it into EU-required formats. CBAM’s proposed expansion to 180 downstream products by 2028 is also drawing in manufacturers that had assumed they were out of scope.

As a starting point, Hu recommended mapping top EU-exported products to their CN codes, the EU’s product classification system used to determine CBAM coverage, and then comparing country-level default values with actual facility emissions. The gap between the two defines the investment case for verified data infrastructure, whether the priority is to reduce near-term certificate costs or to prepare for scope expansion.

On site selection, Loza highlighted permitting ease and the quality of engagement with local authorities as the most critical variables. He also pointed to Vietnam’s strong GDP growth outlook as a sign that broader economic momentum will continue to attract the institutional support, policy coordination, and investor confidence needed to sustain renewable energy commitments.