Operation mechanism

Any business with annual carbon emissions equal to or exceeding 2,000 tonnes of carbon dioxide equivalent (direct emissions) is responsible for registering as a reportable organization and submitting an annual emissions report.

Any major emitter that emits more than 25,000 tonnes of greenhouse gases (GHG) per year must be registered as a taxable enterprise. In addition to submitting a monitoring plan and emissions report every year, a carbon tax of 25 Singapore dollar per ton of GHG emissions should be paid and will be used for energy promotion.

Legal source: the Carbon Pricing Act (CPA)

Carbon taxpayer

About 50 major carbon emitters (over 25,000 tonnes per year) are required to pay a carbon tax, including power plants and semiconductor companies, accounting for 80% of total emissions of Singapore. The nation is one of the countries with the highest carbon tax coverage in the world (Singapore's GHG emissions take up 0.1% of the world's total).

Schedule and content of tax filing

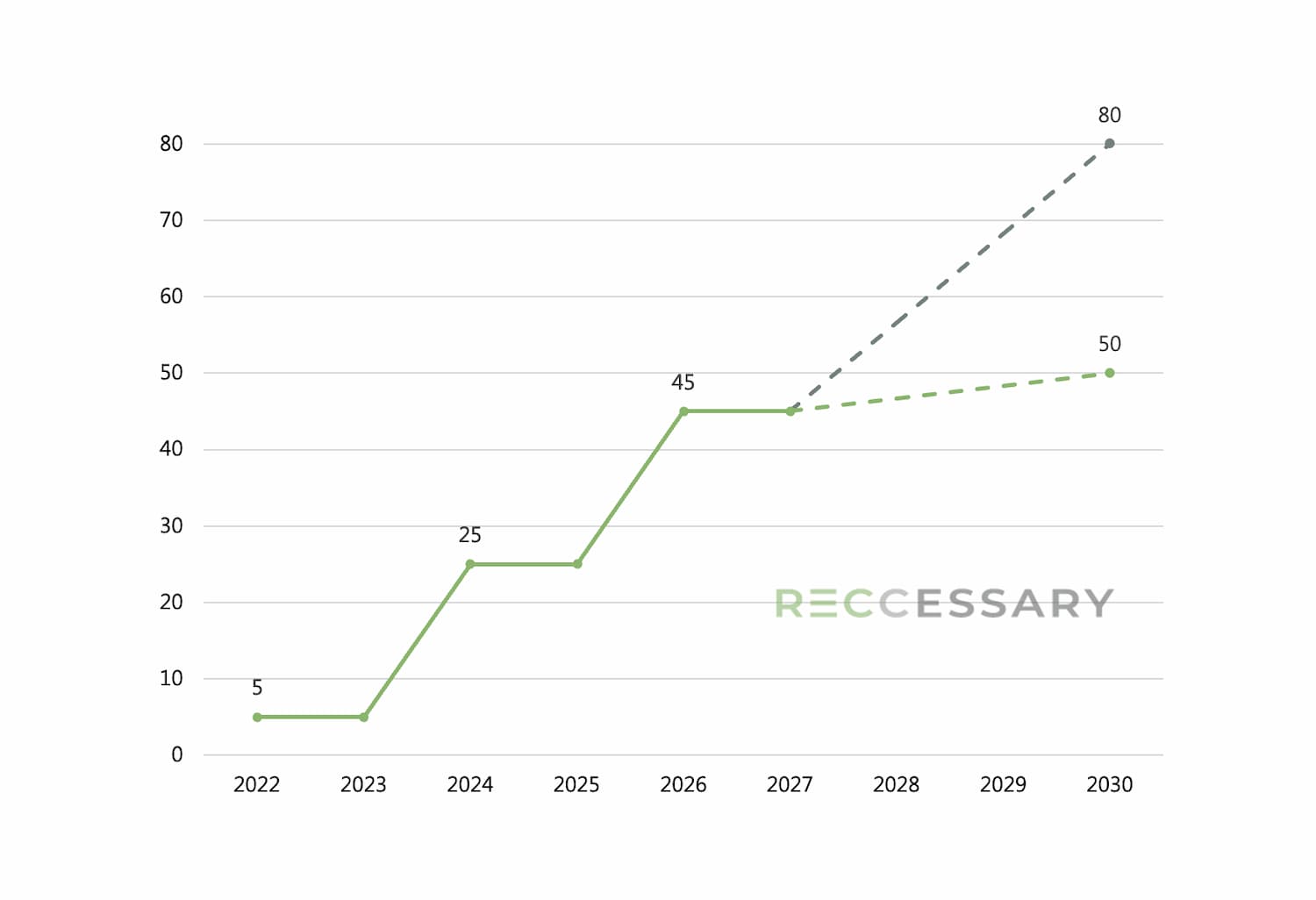

The Singapore government has levied a carbon tax since Jan. 1, 2019 and provided a transitional period until 2023. The current plan is to raise the carbon tax to S$25/tonne in 2024 and S$50-80/tonne by 2030 at the latest.

Figure 1: Singapore’s carbon tax timeline

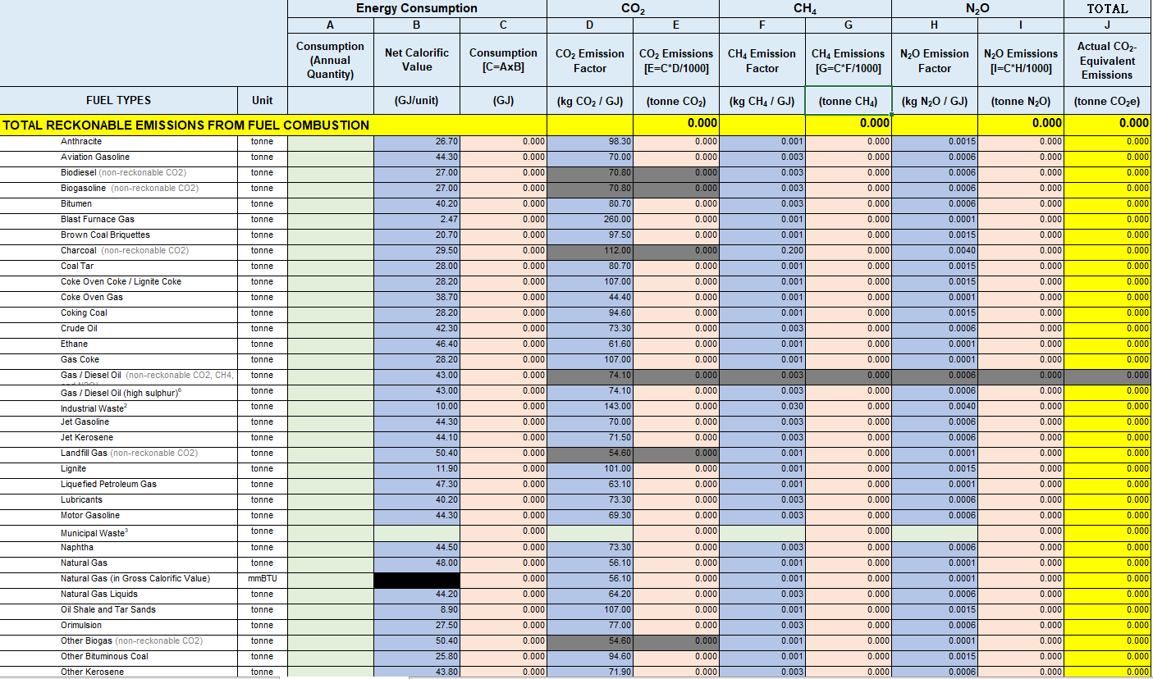

The table for GHG emissions calculation provided by the National Electricity Market of Singapore (NEMS)

GHG emissions measurement and reporting requirements

Report content: The annual emissions report should include activity data, calculation of each direct GHG emissions and total direct GHG emissions.

Report submission deadline: The emissions information of the previous year should be submitted before June 30 of the following year and must be verified by a third-party verification agency accredited by the NEMS before submission.

CPA exclusions:

-

Indirect emissions (Scopes 2 and 3), meaning that electricity consumption does not need to be counted.

-

Emissions from land activities, as defined by the UNFCCC.

-

Transportation emissions.

Verification and accreditation requirements

Reports submitted by all taxable enterprises (emitters of GHG emissions exceeding 25,000 tonnes per year) must be verified by a third-party agency accredited by the NEMS. The verification projects include information related to calculable GHG emissions. The NEMS provides templates for verification notice, verification plan summary and verification report, and verification agencies must conduct the verification according to the templates.

Verification agencies accredited by NEMS:

- Ernst & Young LLP

- PricewaterhouseCoopers LLP

- DNV Business Assurance Singapore Pte Ltd

- TÜV SÜD PSB Pte Ltd

- KPMG Services Pte Ltd

- SOCOTEC Certification Singapore Pte Ltd

- RSM Risk Advisory Pte Ltd.

- Lloyd's Register Quality Assurance Limited

- TEMBUSU Asia Consulting Pte Ltd

- TUV NORD (Thailand) Ltd (Singapore Branch)

Development

In addition to the carbon tax, Singapore is also planning to issue its first sovereign green bond and establish a cross-border carbon credit trading platform – Climate Impact X (CIX). Consisting of Temasek Holdings, DBS Bank, Standard Chartered and Singapore Exchange, the platform is expected to meet various types of demand from multinational corporations and institutional investors through satellite monitoring, machine learning and the blockchain technology.

Sources

- National Environment Agency of Singapore

- Taipei Representative Office in Singapore

- Taipei Forum "Development of Carbon Pricing Mechanism in Southeast Asia"

Update: February 19, 2024