Operational mechanism

Benchmarking as a transitional market mechanism

China’s ETS was initially launched in the power sector and has gradually expanded to multiple carbon-intensive industries. It currently covers four major sectors:

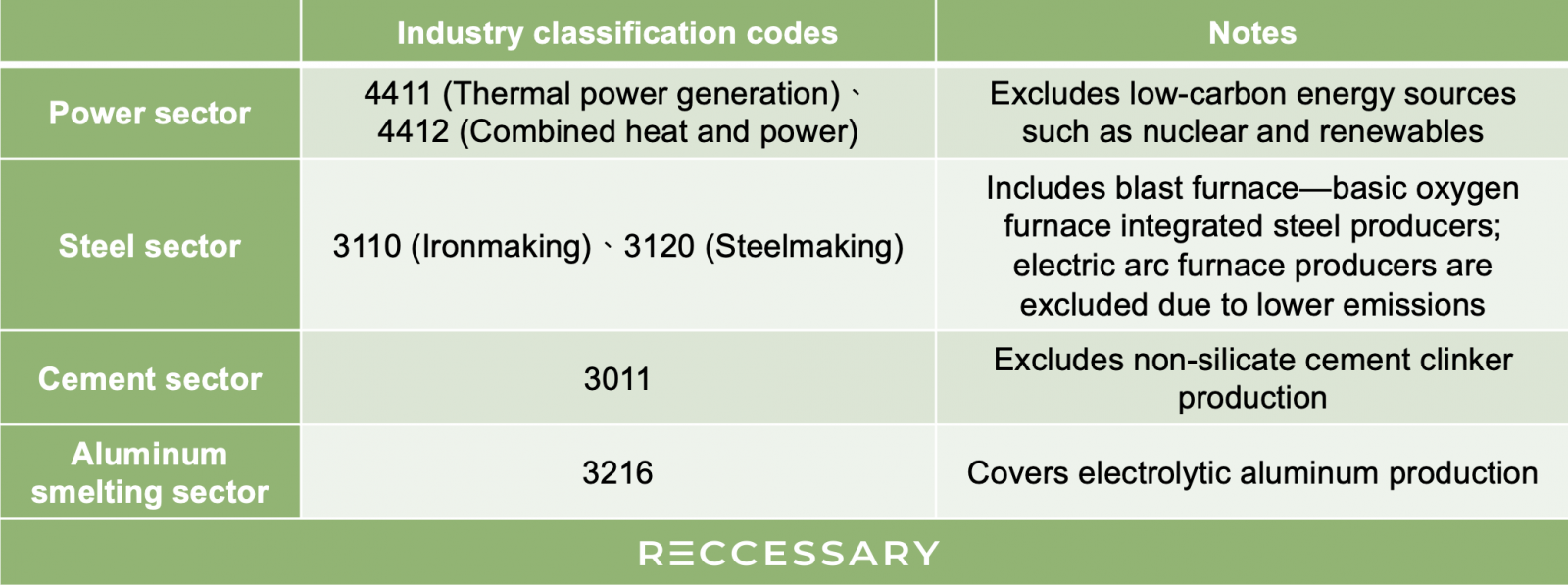

- Power sector: Covers key emitting entities that own generating units. Allowances are calculated using a benchmarking approach, with adjustments made for specific unit-level exemptions and technical characteristics.

- Steel, cement, and aluminum smelting sectors: Coverage for these industries is limited to emissions from fossil fuel combustion and industrial processes, excluding indirect emissions such as electricity and heat consumption.

Unlike conventional cap-and-trade systems, which set an absolute emissions cap, China adopts a benchmarking approach. Allowances are determined based on industry benchmark values and the emissions intensity of individual firms.

Although the benchmarking approach is often criticized for allowing allowance volumes to expand alongside increases in sector carbon intensity, it can also be viewed as a more conservative and gradual regulatory mechanism for large economies that are continuously expanding coverage.

Development of the national system through regional pilot programs

In addition to the national ETS, China approved seven regional pilot carbon markets in 2011, covering Beijing, Tianjin, Shanghai, Chongqing, Guangdong, Hubei, and Shenzhen. Fujian later launched its own pilot system in 2016, becoming the eighth pilot region.

These pilot programs provided experience in monitoring, reporting, and verification, enabling the central government to better understand sectoral differences and local implementation capacity. This helped reduce policy implementation risks and laid the foundation for the official launch of the national emissions trading system in 2021.

Allowance allocation and compliance process

The annual process of China’s emissions trading system consists of three main stages: allowance allocation, allowance surrender, and allowance carryover.

Allowance allocation

- Allowance allocation: Allowances are distributed based on 70% of a company’s emissions in the previous year. This pre-allocation ensures that companies hold a certain volume of allowances before final allocation, enabling early market participation and enhancing market liquidity.

- Final allocation of allowance: Allowances are finalized based on verified annual emissions data from covered entities. Adjustments are made to the pre-allocated amounts based on verified emissions:

1. If final allocation < pre-allocation: the company must return surplus allowances.

2. If final allocation > pre-allocation: additional allowances are issued to the company.

Allowance surrender

According to previous allocation plans issued by the Ministry of Ecology and Environment (MEE)[1] and the latest notice for 2026[2], covered entities are required to surrender allowances equivalent to their verified emissions by December 31 each year, as specified in the compliance notice.

Up to 5% of compliance obligations may be met using China Certified Emission Reductions (CCERs), in accordance with relevant regulations.

Allowance carryover

After compliance obligations have been fulfilled, any remaining allowances may be carried forward to the following year, subject to applicable regulations. Carryover rules are announced by the regulatory authority for each compliance period. At present, the system allows relatively flexible carryover to maintain market liquidity and provide price support in the carbon market.

Timeline

Development timeline of pilot regions

China approved seven regional pilot programs in 2011. Shenzhen became the first pilot to launch in 2013, followed by the inclusion of Fujian as the eighth pilot region in 2016.

Development timeline of the national carbon market

In 2017, the MEE released the Program for the Establishment of a National Carbon Emissions Trading Market (Power Generation Industry), marking the formal launch of the national ETS framework.

In 2020, President Xi Jinping announced China’s “dual carbon” targets, one of the most significant climate policy initiatives in recent years, which has since served as the overarching policy direction across government sectors.

In 2021, one year after the announcement of the dual carbon targets, China officially launched its national ETS, initially covering only the power sector.

In 2025, the system expanded to include the steel, cement, and aluminum smelting sectors. About 1,500 additional covered entities were incorporated, increasing total coverage by around 3 billion tonnes of CO2 equivalent.

Coverage and participation

Starting from 2025, the inclusion of the steel, cement, and aluminum smelting sectors, together with the existing power sector, expands the system to cover more than 3,500 enterprises. Total coverage reaches around 8 billion tonnes of CO2 equivalent annually, accounting for about 60% of China’s total carbon emissions.

Covered entities are defined as key emitters with annual direct emissions of at least 26,000 tonnes of CO2 equivalent. Sector classification for covered entities is determined based on national economic industry classification codes.

Table 1. Industry classification codes for covered sectors

Trading instruments and venues

Carbon emission allowances (CEAs) are traded through the official trading system. Transactions may take place via block trading, one-way bidding, or other compliant mechanisms. Block trading includes both listed agreement transactions and large-scale negotiated trades. The market is primarily based on spot trading of carbon allowances, while derivatives such as carbon bonds, options, and pledged carbon assets remain at the regional pilot stage, including markets in Beijing, Tianjin, Shanghai, Chongqing, Guangdong, Hubei, and Shenzhen.

The national trading platform is the Shanghai Environment and Energy Exchange, which operates as a unified market and is responsible for account registration, trading system operations, and maintenance. Regional pilot markets continue to operate through their respective exchanges, such as the Shenzhen Emissions Exchange.

Carbon price

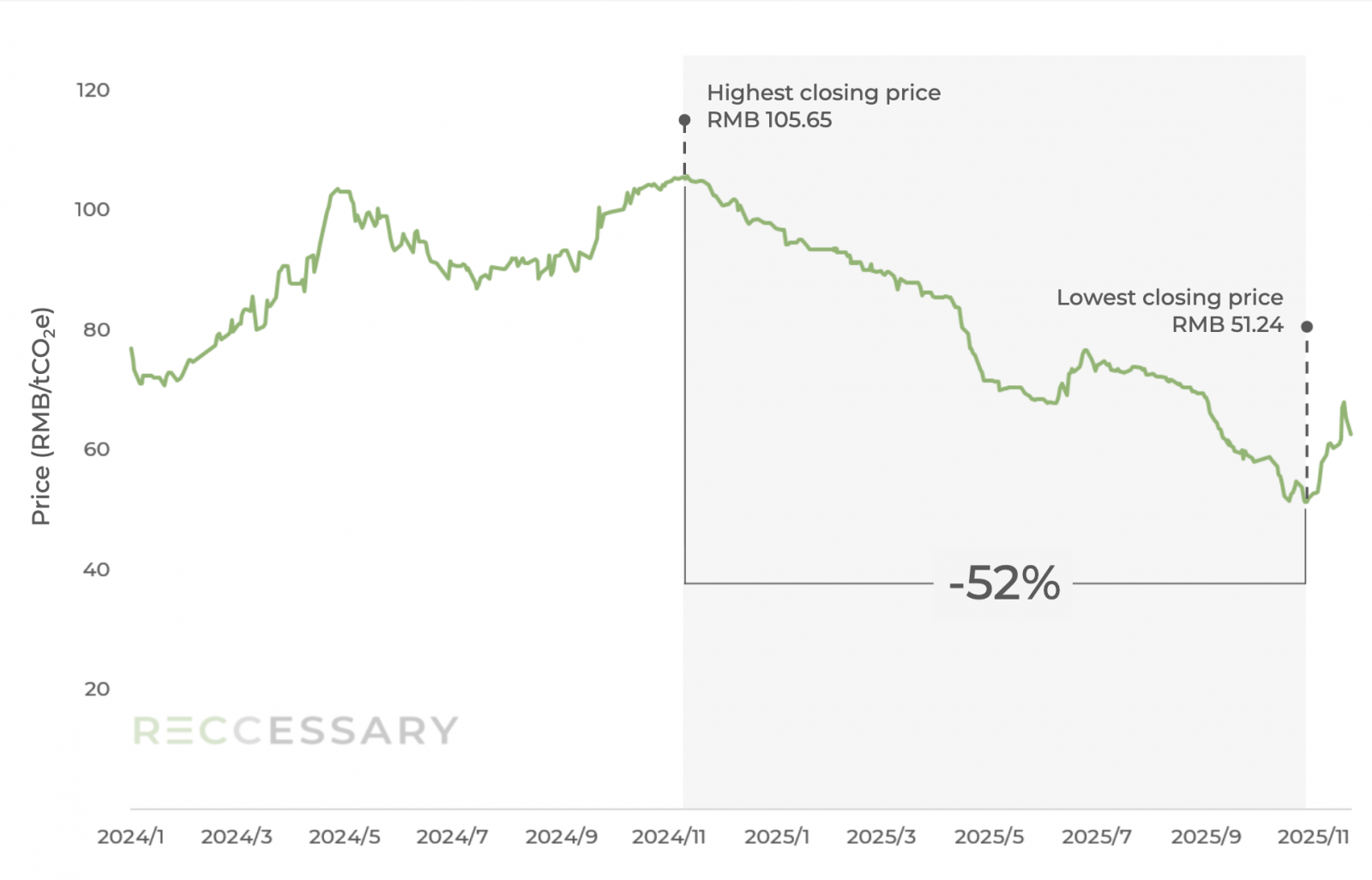

Figure 1. CEA price trend

Over the past two years, CEA prices rose from around RMB 70 per tonne to above RMB 100 by the end of 2024, driven by expectations of expanded sector coverage. However, large-scale allowance allocations and the absence of a binding emissions cap led to a subsequent decline in prices.

In November 2025, the MEE released a new allocation plan for additional covered sectors. Renewed market expectations of system expansion helped restore buyer confidence, stabilizing prices and triggering a rebound in CEA levels.

At present, CEA prices remain largely influenced by administrative announcements, allocation policies, and changes in sectoral coverage. Looking ahead, the introduction of an absolute emissions cap would be a key factor in aligning carbon prices more closely with underlying emissions demand.

Future developments

A tightening carbon market framework

President Xi has indicated at the Asia-Pacific Economic Cooperation (APEC) forum that China will move toward a dual control system combining an emissions cap with intensity-based targets. At the same time, the MEE is accelerating the transition toward paid allocation of allowances and gradually tightening allocation levels.

Expansion of additional sectors

The MEE has initiated the development of supporting technical frameworks for additional industries, including chemicals, petrochemicals, civil aviation, and paper. These efforts include allocation plans, emissions accounting guidelines, and verification standards. The goal is for the national ETS to cover major industrial emitting sectors by 2027.

Source

[1][2]2023、2024年度全国碳排放权交易发电行业配额总量和分配方案/2024、2025年度全国碳排放权交易市场钢铁、水泥、铝冶炼行业配额总量和分配方案/关于做好2026年全国碳排放权交易市场有关工作的通知

Updated: 2026/4/14