Geothermal energy investment potential in Indonesia

Both Indonesia and the Philippines have abundant geothermal resources. Indonesia, in particular, has the greatest potential in Southeast Asia. Nevertheless, the Philippines has seen rapid development of geothermal energy in terms of both policies and incentives, making the existing installations and the geothermal energy market mechanism more comprehensive than in Indonesia. The Philippines develops geothermal energy through auction mechanism as its market is relatively mature. In 2021, the Department of Energy of the Philippines completed its third round of Open and Competitive Selection Process (OCSP), in which five potential sites with a total capacity of 218 MW were put out for tender. However, two of the smallest sites[1] did not receive bids and they might be included in the fourth round of OCSP in 2023, as the investment incentives for small sites are still under discussion.

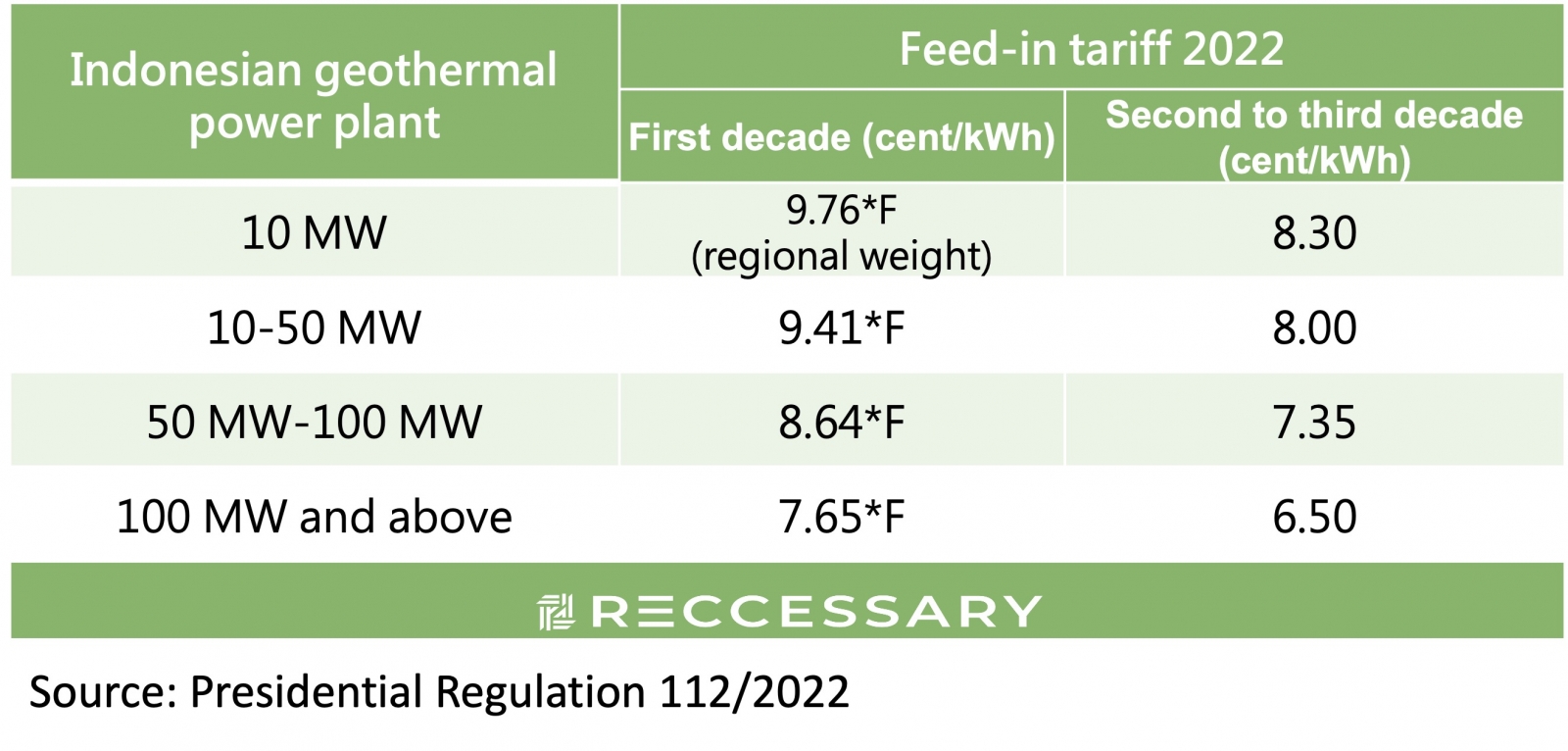

Table 1. Feed-in tariff for geothermal energy in Indonesia

Indonesia is quite active in introducing policies for geothermal investment and development. The first was the Presidential Regulation 112/2022 announced in mid-2022, which published the updated feed-in tariff for geothermal energy, with higher rates than in previous years and geographic factors considered (as shown in Table 1 above). In addition, the Indonesian Ministry of Energy and Mineral Resources (ESDM) is expected to issue bids for two geothermal energy sites, namely Way Ratai WKP and Nage WKP, by the end of 2022. Nage WKP is one of the sites in the government's drilling program, which suggests that private developers will not have to bear the cost and risk of drilling and will be a significant investment incentive. Next, Indonesia's bulk purchase rate will be used as a scenario benchmark for investment calculations. The following investment simulation will be based on the feed-in tariff of Indonesia.

The cost of geothermal energy development can be divided into two categories. First is the overall construction cost. As mentioned above in the process of geothermal power generation, the cost of civil engineering works such as preliminary project development, site preparation, well construction, and power plant construction is quite high. In addition, drilling costs for geothermal energy are affected by the international oil and gas industry cycle, which will have a direct impact on engineering, procurement, and construction (EPC) cost. The overall construction costs are highly sensitive to the location of development and the quality of the geothermal reservoir, making it difficult to estimate costs in a standardized manner similar to solar and hydro. The overall construction cost in the following investment simulation is based on the average capacity data from the International Renewable Energy Agency (IRENA) and the Indonesia Geothermal Association. Yet, this estimate is not applicable to all Indonesian geothermal energy development projects

The other cost is the maintenance cost. A high proportion of the maintenance cost of geothermal energy is for the maintenance of wells. Over time, the pressure in the reservoir around the wells decreases, resulting in lower flow rates. If maintenance is not performed, the efficiency of power generation will be significantly reduced and all equipment may even be scrapped, making the maintenance cost of geothermal energy higher than other renewable energies. The overall cost of geothermal energy is high, so is its efficiency of power generation. Since electricity can be generated from geothermal energy 24 hours a day with an average capacity factor of about 80% to 94%, the capital of geothermal energy can be recovered quickly. In addition, Indonesia and the Philippines offer many financial incentives for geothermal energy, such as tax exemptions on imports of foreign equipment and low interest rates on financing, which significantly lower the capital threshold for investment in geothermal energy.

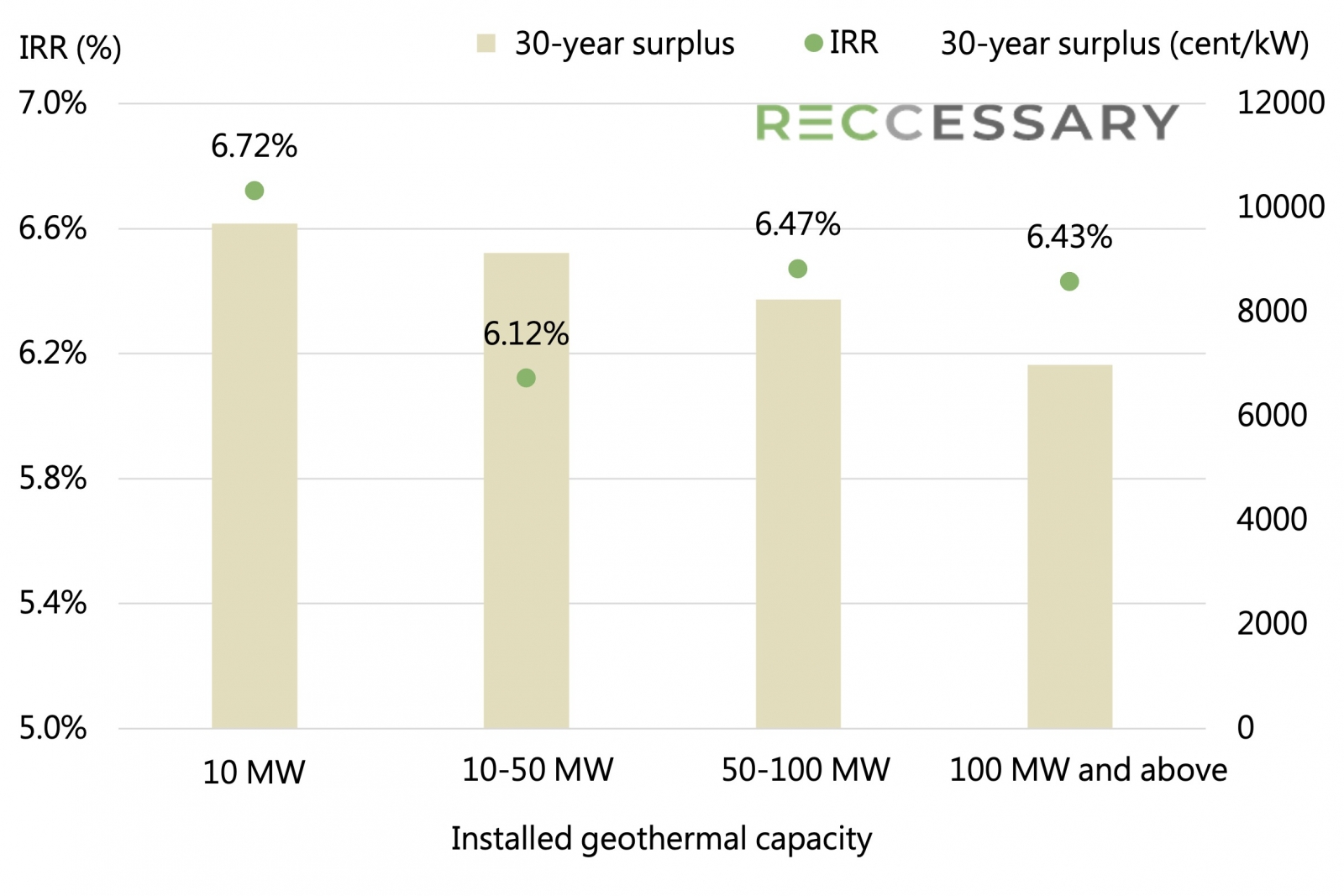

Figures 1 below shows the IRR and 30-year surplus per kW by capacity range of the feed-in tariff, based on the cost side (overall construction cost and maintenance cost) and revenue side (feed-in tariff) of geothermal energy in Indonesia. There is no significant difference in IRR in terms of capacity range, while the 30-year surplus per kW decreases gradually with increasing installed capacity. Despite the quicker return on capital for small-scale installations, each geothermal site development entails significant risk, making it favorable to develop sites with larger capacity rather than dozens of small sites. For example, developers would prefer to invest in a 60 MW site rather than six 10 MW sites. This is the main reason why the smallest two sites in the Philippines did not receive any bids in the third round of OCSP.

Figure 1. IRR and 30-year surplus per kW of thermal energy installed capacity in Indonesia in 2021

Many companies do not dare to engage in geothermal energy technology as preliminary development of geothermal energy is time-consuming, costly, and high-risk. However, in recent years, more and more governments have taken on the risk of comprehensive geothermal resource mapping and drilling, providing the development information to the winning bidder, which has significantly increased the willingness of private investment. While advanced development technologies will significantly reduce production costs, as geothermal energy is in a transitional period of technology over the next five to ten years, the cost of global geothermal installations is of particular concern to many investors and developers.

[1] The two sites are Makban Geothermal Plant and Binary Geothermal Plant (4 MW) and Tongonan 1 Geothermal Plant (9 MW).