Green finance: a catalyst facilitating energy transition

In the face of escalating climate change, energy transition has become an urgent issue, which should be addressed through shifting towards sustainable and environmentally friendly energy sources. During the transition process, green finance plays a key role in achieving the goals. Green finance is financial activities taking into consideration environmental aspect, aiming to channel capital to eco-friendly projects and business (e.g., green energy and green technology) to promote environmental protection and sustainability, addressing climate and environment-related issues.

Energy transition requires substantial and stable investment to support the research and development, construction, and promotion of new energy sources. However, traditional finance often favors the traditional energy industry, which makes it difficult for green energy projects to receive adequate financial support. This shortfall is addressed by the emergence of green finance, which introduces specialized financial institutions and products to facilitate the financing for green energy projects and accelerate the energy transition. In addition, green finance contributes to improving energy efficiency and reducing emissions. One of the goals of energy transition is to reduce reliance on carbon-intensive energy sources and shift to green energy. By supporting energy-saving technologies and clean energy development through green finance, businesses and individuals are able to adopt energy-saving and emissions reduction solutions more easily, thereby reducing greenhouse gas emissions and effectively addressing climate change.

The development of green finance varies between countries and partly reflects the progress of their energy transition and future development. This article will provide insights of the current situation and challenges of green finance development in the five Southeast Asian countries (hereinafter referred to as ASEAN-5): Malaysia, Thailand, Indonesia, Vietnam, and the Philippines.

Green bonds in Southeast Asia

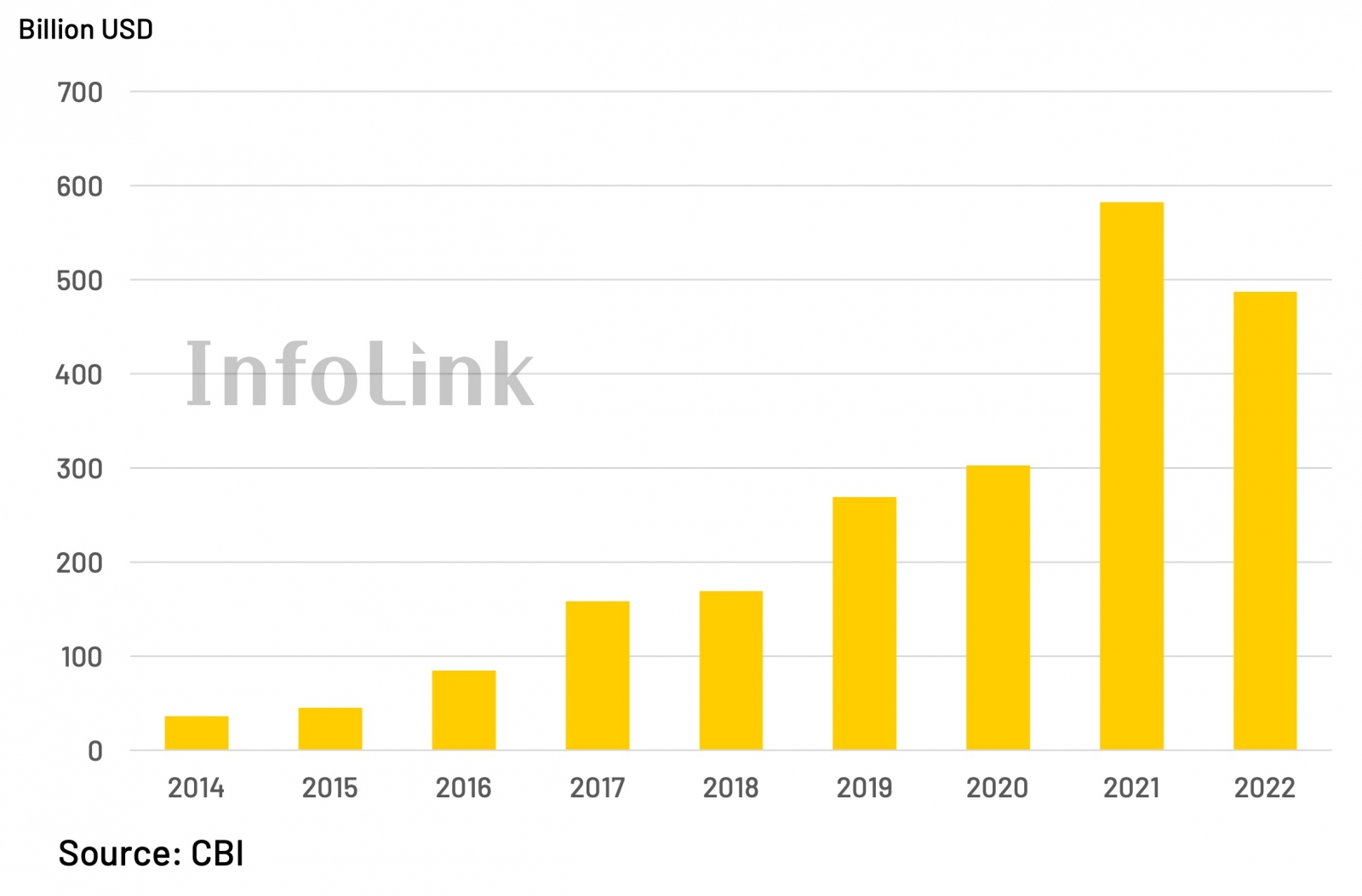

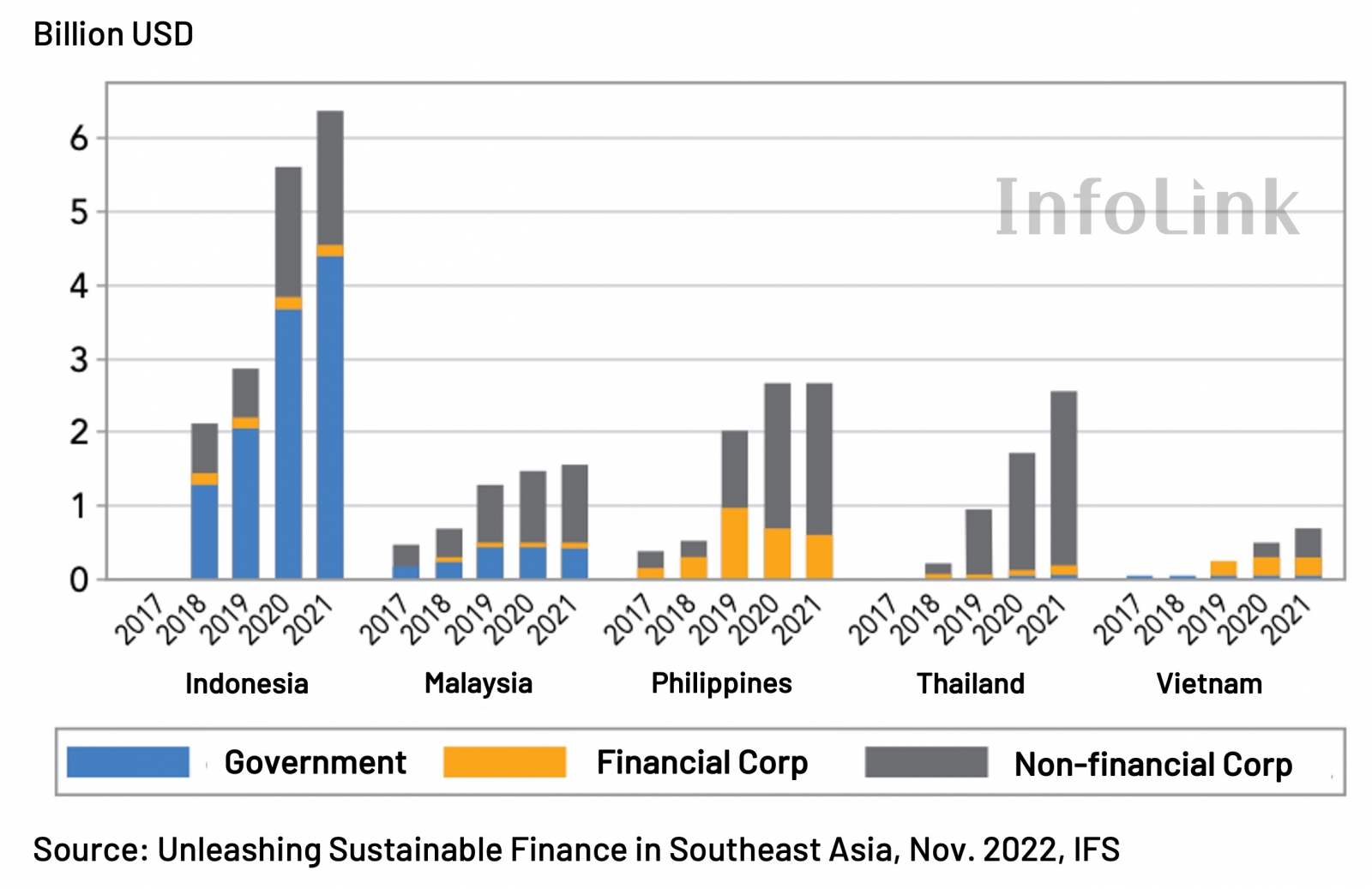

Since 2017, the scale of global green finance market has been growing over the years. According to the Climate Bonds Initiative (CBI), global green bond issuance amounted to US$158.6 billion in 2017. In 2022, the total reached US$487.1 billion, a growth rate of 207%, despite a slight decline from the peak in 2021 (see Figure 1 below). Among ASEAN-5, Indonesia is the largest green bond issuer from 2017 to 2021, with over 60% of issuance before 2021 dominated by the government, a proportion higher than the other four countries. During these five years, more than 70% of Malaysia's green bonds were issued by corporations, while the Philippines, Thailand, and Vietnam had all their issuances from corporations, with no government involvement[1].

Figure 1. Global green bond issuance, 2014-2022

Figure 2. Green bond issuance and mix in ASEAN-5, 2017-2021

The participation ratios of governments and businesses in the green bond market reflect the market attitude towards environmental issues. Green bonds and sustainable bonds issued by governments play the role of market pioneers, while higher corporate participation indicates market confidence in the trend. Currently, only 51 companies in ASEAN-5 engage in green and sustainable bond issuance, of which 31 are non-financial institutions, a participation ratio of 0.18 companies per million population, compared to the world's average of 1.76 companies per million population. Among them, Malaysia's corporate participation in green bonds stands at 0.6 companies per million population, the highest among the five countries and ranked 64th globally, though it still falls towards the lower end.

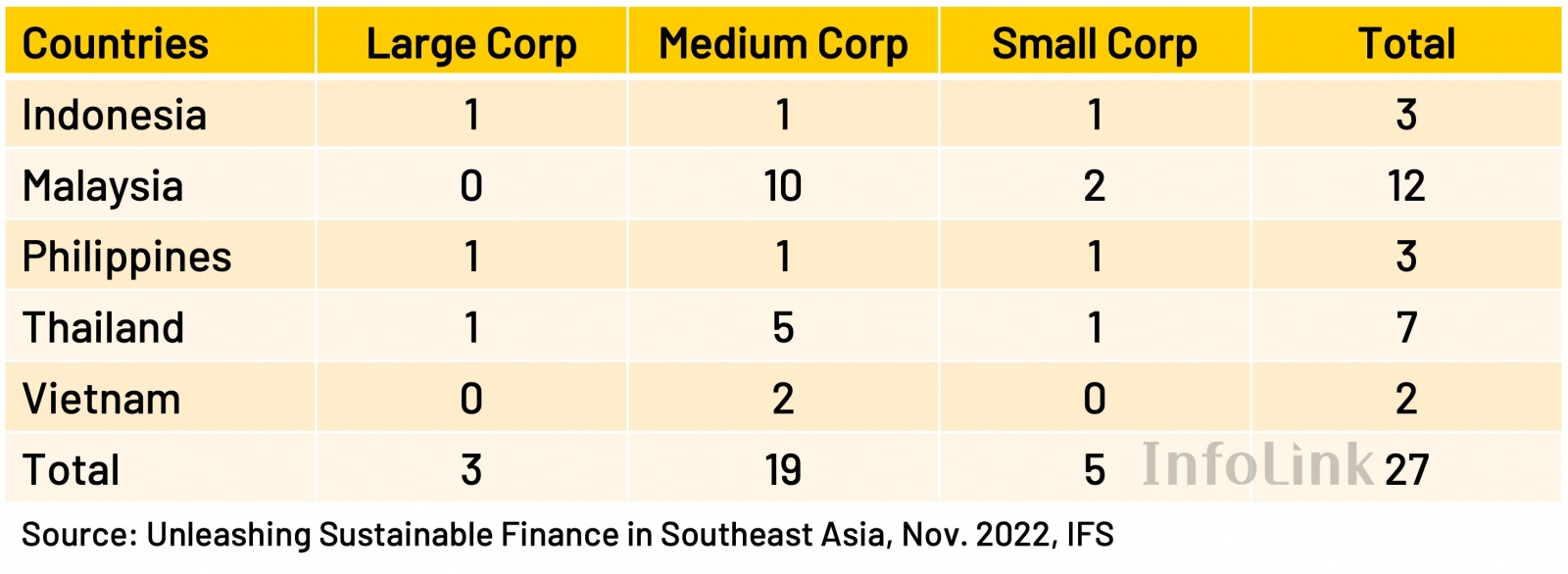

Table 1. Green bond issuance for non-financial corporations in ASEAN-5, 2017-2021

In terms of credit ratings, 80% of green bonds issued in Southeast Asia between 2017 and 2021 were rated Baa by Moody's Credit Ratings, with the remaining 20% rated Ba[2]. However, more than 70% of non-financial corporations prefer bonds rated Baa or above, suggesting that green bonds in Southeast Asia are almost at the bottom of the corporate investment scale. Nevertheless, the performance of ASEAN-5 and other Emerging Market and Developing Economies (EMDEs) remains relatively favorable. Apart from China, 56% of the EMDEs are below the corporate investment threshold (Baa).

Green bond issuance in ASEAN-5

Among the ASEAN-5, although Indonesia has issued the highest amount of green bonds, Malaysia is the most active country engaging in the market, with its corporations contributing to over 40% of the overall ASEAN-5 green bond market. In addition, Malaysia has issued the largest number of Islamic green bonds (Green Susuk) in the ASEAN reigon.

reNIKOLA is a Malaysian solar developer with a total of 415 MW of solar asset portfolio. The company participated in the ASEAN Green SRI Sukuk Programme in 2021, which aims to set up an additional 88 MW of large-scale power plant projects. They issued green bonds worth RM 390 million, which were rated AA3 by RAM Ratings, classifying it as stable bonds, with a holding period ranging from 1 to 17 years and set to mature in 2038.

Barriers to green finance markets in ASEAN-5

There are two major concerns for companies investing in the ASEAN-5 green market: unclear market information and resource constraints. When making investments, companies need to fully understand local green industry trends, government policies, and environmental regulations to develop effective business strategies and risk assessments. However, some Southeast Asian countries do not have well-established environmental regulations, which may result in investment risks for companies in the absence of a clear market outlook.

On the other hand, investing in emerging green markets such as ASEAN-5 requires significant capital, time, and human resources, as well as efforts including conducting market research, establishing local partnerships, and promoting products and services, all of which require long-term commitment and investment. However, due to limited resources, companies may have to prioritize other projects and postpone cross-border green investments.

InfoLink's Southeast Asia market analysis

With long-term research on the Southeast Asia sustainable market, InfoLink Consulting provides customized reports tailored to specific business needs to address the challenge of opaque market information. The reports features in-depth insights, comprehensive market intelligence, opportunity analysis, and risk assessment, enabling companies to gain a more comprehensive understanding of a region's green industry development for investment purposes. In addition, InfoLink Consulting employs various scenario analyses to simulate future revenue curves, helping enterprises evaluate returns, mitigate risks, and develop suitable market strategies for different situations, thus assisting them in achieving sustainable and robust development in Southeast Asia.

[1] The governments of Thailand and Malaysia have been actively investing in sustainable bonds in recent years. Sustainable bonds include a broader scope than green bonds, supporting not only green energy-related projects but also social and economic sustainability, such as green buildings.

[2] Source: SDC data