.jpg)

(Photo: REM)

The annually held Renewable Energy Market (REM) Asia commenced in Singapore on April 28. The conference provided a valuable opportunity for governments, businesses, and research institutes to gather and discuss the latest market and policy developments of renewable energy demand and supply in Asia.

Spinning off from the major themes from the event, this article expands on discussions that took place and incorporates our own analyses for market trends and recommended green power purchase corporate strategy. There are two important takeaways from this conference, 1) options and accessibility for green power is determined by the status of cross-border trading and national market supplies; and 2) MNCs need nuanced strategies for corporate green power procurement options. The following section will first provide an update on the market status of selected Asian countries.

Varying corporate green power procurement options

Markets in Asia are adopting varying sets of green power procurement options at different pace. In general, the most commonly used scope 2 decarbonization mechanism in the region remains unbundled RECs. That said, confronted by growing concerns over additionality and double counting, when presented with the opportunity under the right conditions, alternatives for green power procurement with higher additionality are increasingly welcomed. It is then imperative to understand what is available where, as well as the main barriers for corporate participation. The sections below will be a glimpse of the updated status of markets in different Asian countries.

1. South Korea

The biggest challenge the companies face in the country is low supply and high cost of renewable energy. Currently available green power procurement options in South Korea include green premium, direct PPA, self-consumption, and REC purchase. Businesses in the country tend to purchase Green Premiums, the most inexpensive option, for sustainability claim. Green Premium, however, are associated with greenwashing risks. Meanwhile, corporates appear to be showing greater interests in reaching green power purchase deals at the stage of power project development in hopes to secure higher quality green power in the future.

2. Vietnam

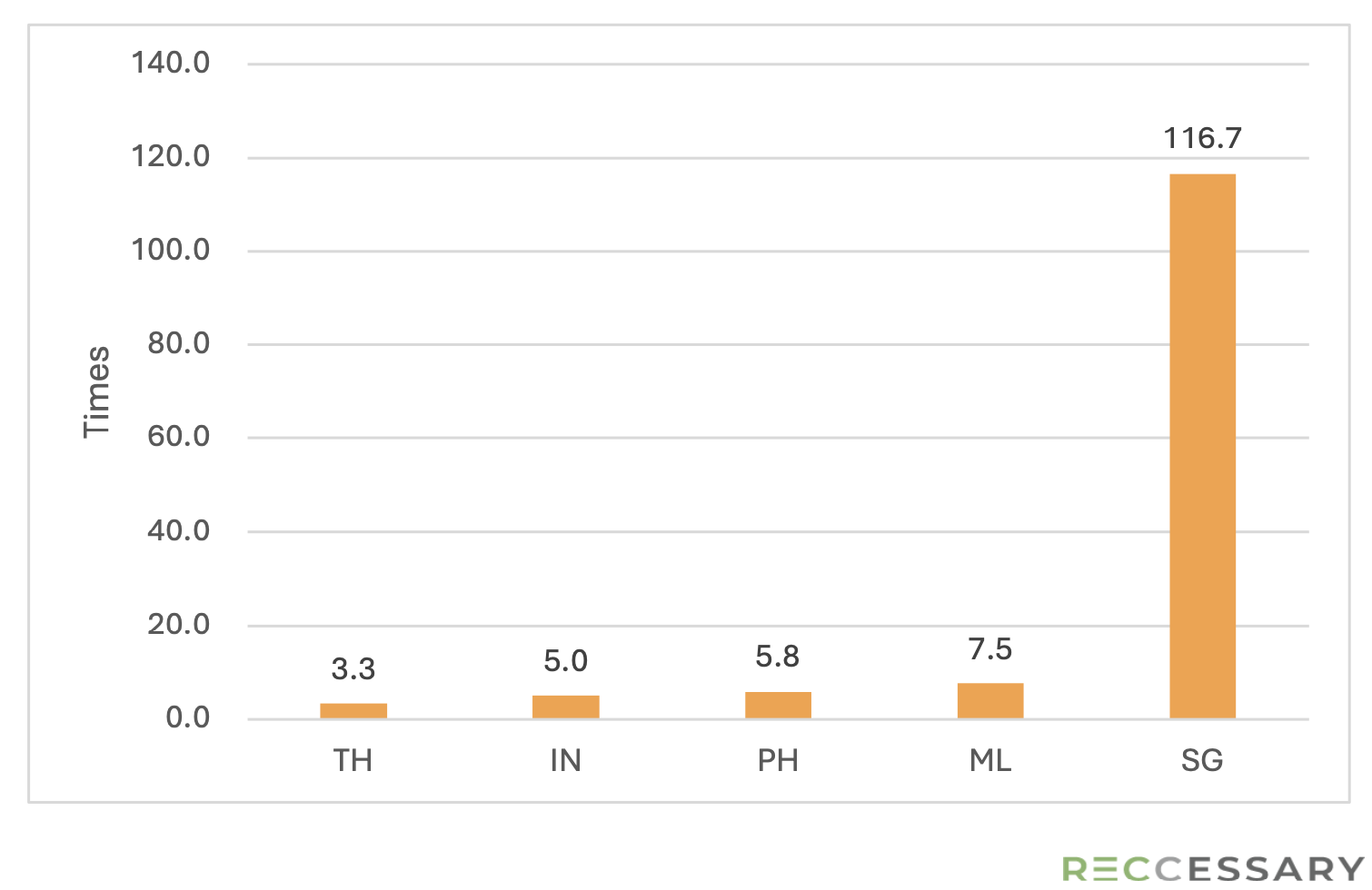

Leading the region in renewable energy development, Vietnam is currently the biggest supplier of the cheapest RECs in Southeast Asia. In fact, REC prices in neighboring countries are at least three times that of Vietnam’s (Figure 1). Unfortunately, apart from unbundled purchase of certificates, progress in opening additional procurement channel in the country has been slow. The direct PPA (DPPA) pilot project that began drafting in 2022 is expected to be implemented on July 1 this year. Corporate users that follow stringent locality rule will not be able to tap into Vietnam’s cheap supply and may need to opt for rooftop leasing before the full implementation of DPPA.

Figure 1. I-REC/TIGR prices compared to Vietnam

3. Singapore

As the most mature electricity market in Southeast Asia and the market with the most significant supply-demand imbalance for corporate green power, the Singaporean government has implemented several initiatives to encourage the development of renewable energy. But due to its limited landmass, the city-state struggles to provide enough supply to match the demand at the current stage. The Singaporean government has been actively seeking power imports from neighboring states such as Indonesia and Malaysia through the regional power grid. The cross-border power trade is expected to bring in more and cheaper power for the energy consumers in the country. A 100MW trial supply of physical solar and hydro power from Malaysia will start in July and 2GW solar power is expected to be imported from Indonesia by 2035.

4. Japan

There are three types of electricity certificates in Japan, but they do not always satisfy the international requirement on identifiable energy sources, posing serious concern for RE100 corporates. Thus far, RE100 only recognizes non-FIT NFCs that meets the organization’s disclosure criteria. VPPA is another viable option in the country, but it also comes with financial risks. When conditions allow, corporates can also choose to sign on-site solar PPA, which not only has high additionality, but also relatively little upfront costs and prices compared with normal electricity tariff.

5. China

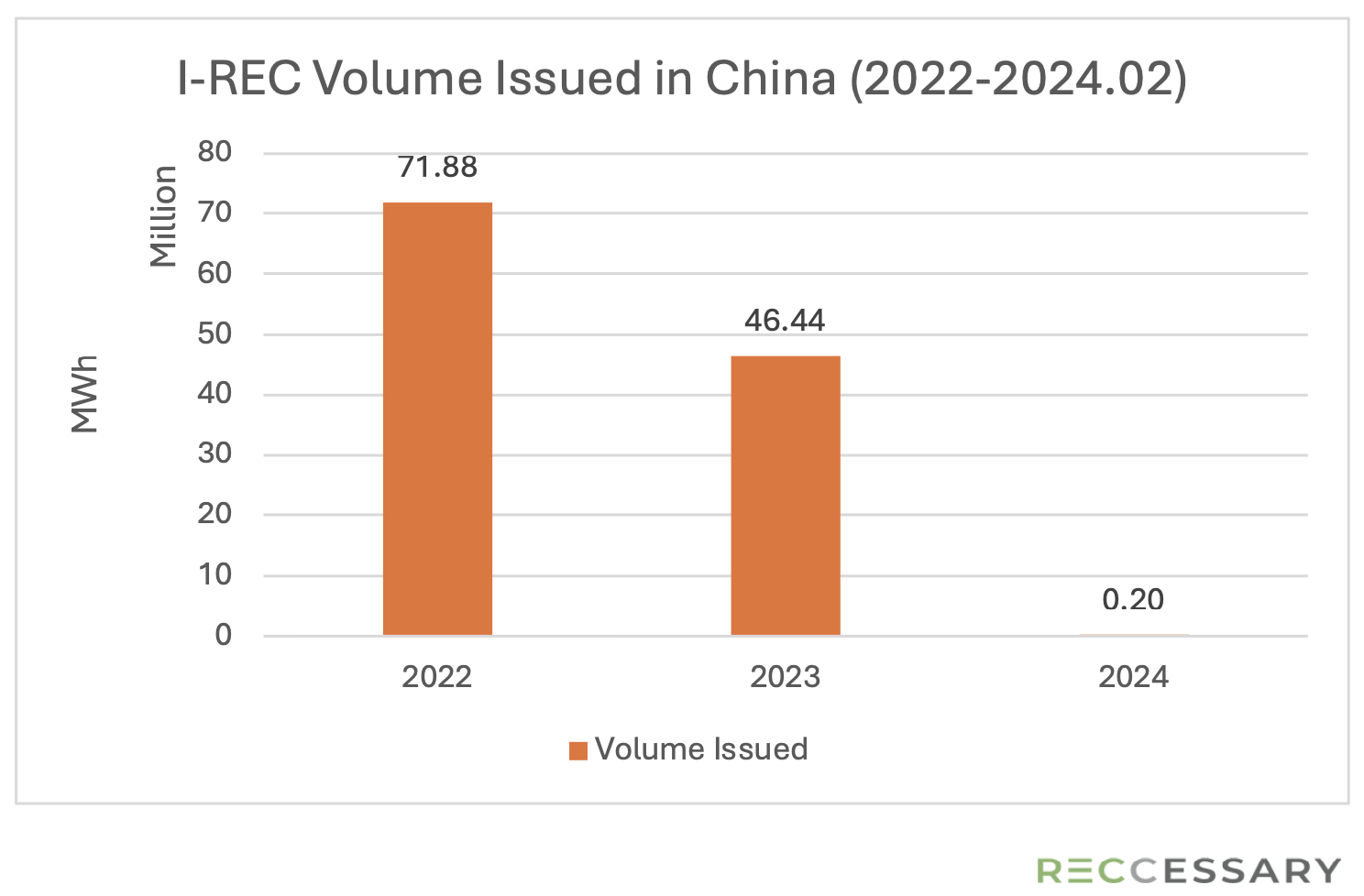

Interprovincial transmission is currently unavailable due to grid limitation, but a document released by the State Council in February aims to enable the practice for foreign investors, signaling a positive trend to grant greater access to green power for businesses in the coming years. Apart from actual electron transmission, the energy certificate market is expected to change as well. As the Chinese government recognizes the domestic REC system – GEC, as the sole tracking system for renewable energy consumption, the use of international RECs is bound to reduce greatly and phase out of the country eventually. In fact, the past two years have shown visible decrease in I-REC issuance in the country (Figure 2).

Figure 2. I-REC volume issued in China (2022-2024.02)

Key takeaways and further recommendations

Market mechanisms are determined by multiple factors from the more tangible conditions of grid infrastructure, the performance of subsidy programs and installed renewable energy capacity, to the more elusive conditions that are harder to gauge like regulatory environment and political stability. It goes without saying how differently Asian countries are doing with regards to these conditions.

One thing that these markets have in common is the dominant use of unbundled RECs and growing corporate interests to move to some form of PPA. This trend is motivated by increasing demand for additionality and public supervision on greenwashing behaviors. Company decisionmakers are now tasked with the responsibility to make a weighted judgement on costs and additionality. With different sets of available options in different markets, matching one’s business’ capacity and needs is not an easy hurdle.

But at the end of the day, the first step to make a decision is always checking your reporting venue, or whether your clients or your organization are following any voluntary standards. An undergoing trend for scope 2 decarbonization is stricter rules around time-matching and locality of energy use. Additionality of green power production is another growingly important aspect of decarbonization evaluation. Understanding criteria on these two fronts will save companies on potential loss of green competitiveness and greenwashing accusations.