.jpg)

Southeast Asia’s subsea cables are a key element for achieving the regional target of achieving 45% renewable energy capacity by 2030. (Photo: iStock)

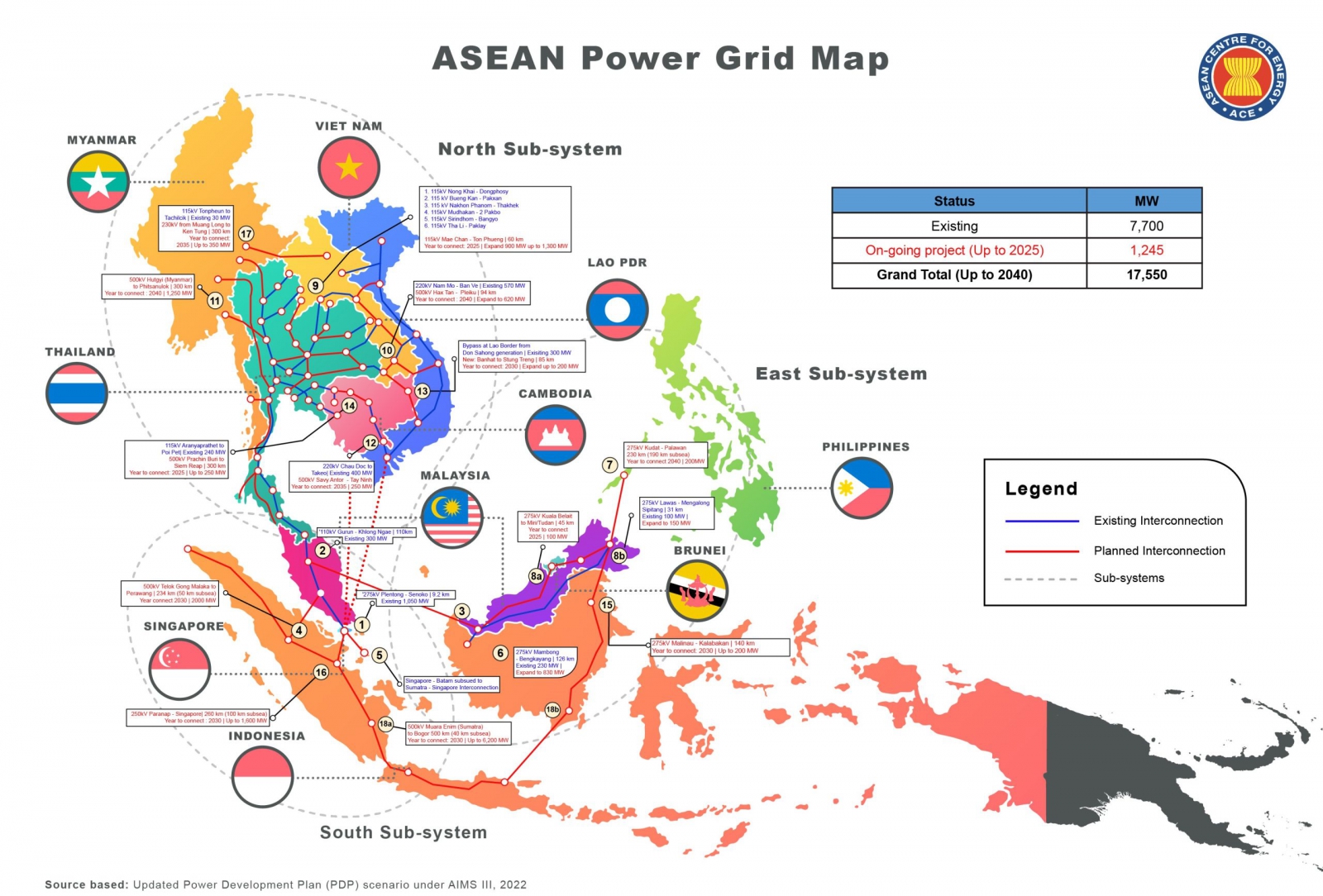

The ASEAN Power Grid (APG) has entered a new era of unprecedented momentum. For the first time in nearly 30 years since APG was launched, sustained political support is driving concrete progress on cross-border grid initiatives. In the last three years, ASEAN has achieved two breakthroughs that has been out of reach for almost three decades: the shift from purely bilateral electricity trading to a multilateral framework[1], and consistent momentum towards the development of subsea power cable projects, which can transform energy trade in archipelagic Southeast Asia.

Currently, as many as six subsea power cable projects are at advanced stages of negotiation and planning (Table 1). Strong and sustained political commitment from regional leaders has been central to contemporary progress. The Joint Statement of the 43rd ASEAN Ministers on Energy Meeting (AMEM) held in Kuala Lumpur in 2025 describes subsea cables as a key building block of the APG and calls for accelerated progress on the completion of the Submarine Power Cable Development Framework, which will inform cooperation on four key priorities: legal and regulatory, technical, commercial, and governance. The Framework is expected to be completed during the 2026 Philippines Chairmanship of ASEAN and will enable the regional bloc to manage the laying, maintenance and repair, and protection of subsea power cables.

Table 1. Subsea Power Cable Projects in Southeast Asia[2]

| Interconnection | Status | Infrastructure | Energy Source | Potential Trade | Length (Approx.) | Completion Date (Approx.) |

| Singapore – Indonesia | Conditional approval, Energy Market Authority (EMA), Singapore | Subsea | Solar | 3.4 GW | — | — |

| Singapore – Sarawak | Conditional approval (EMA) | Subsea | Hydro | 1 GW | 750 km | 2032 |

| Singapore – Cambodia | Conditional approval (EMA) | Subsea | Solar, Hydro, Wind | 1 GW | 1,000km | TBA |

| Singapore – Vietnam | Conditional approval (EMA) | Subsea | Offshore Wind | 1.2 GW | 1,000 km | TBA |

| Vietnam–Malaysia–Singapore | Joint Development Agreement | Overland + Subsea | Offshore wind/others | 2 GW | 700km (subsea) & 782km (overland) | 2034

|

| Australia – Singapore | Conditional approval (EMA) | Subsea | Solar | 1.75 GW | 4,300 km | 2035 |

Southeast Asia’s subsea cables are a key element for achieving the regional target of achieving 45% renewable energy capacity by 2030. While overland cables are just as important, the geographic flexibility offered by subsea cables will have a catalytic impact on regional energy transition by: 1) increasing the numbers of energy buyers and sellers, thereby decreasing risks for both groups; and 2) Spurring green industrialization and economic growth at subnational levels.

Subsea cables that traverse the South China Sea or the Java Sea greatly increase the diversity of suppliers, thereby reducing risks for electricity importers in Southeast Asia. The geographic constraints of land-based infrastructures limit the number of players involved in energy trade arrangements, which can leave energy importers vulnerable to disruptions. Subsea cables can be used to manage such energy security risks. For example, in Europe, Spain’s subsea cables with Morocco help diversify the sources of the country’s electricity imports, which also includes France and Portugal. Such diversification can also be useful during emergencies. During the Iberian Peninsula blackout, Morocco played a crucial role in utilizing its subsea power cables to restore power in Spain.

These projects are also beneficial for Southeast Asian countries that export electricity, as they will no longer need to rely on selling to their immediate neighbouring state. Subsea cables will give them access to new regional markets, more competitive tariffs and higher levels of foreign investment in the energy sector. For example, Norway uses the North Sea Link subsea cable to export excess hydropower to the UK, earning significant revenue through clean energy. Similarly, Vietnam can utilize subsea cables to develop completely new markets in Singapore and Malaysia (table 1), while continuing to use its land-based infrastructures to import and export electricity with Cambodia and Laos.

Another important benefit of subsea cables is that due to their relative novelty, they are being envisioned not as an extension of existing systems, which are based on fossil fuels, but as part of a new renewable energy eco system, which includes not only transmission infrastructures, but also the development of green industries in Southeast Asia. Most of the proposed subsea projects will use solar, wind or hydropower, which will increase regional renewable electricity generation capacity (table 1). In addition, these projects will also facilitate the development of green industries in the region. For example, Singapore’s collaboration with Indonesia includes not only the export of solar energy, but also the development of solar PV manufacturing plants. Cambodia’s cooperation with Singapore involves the development of one of the longest subsea cables in the world, as well as pumped hydro or battery energy storage systems. Vietnam’s collaboration with Malaysia and Singapore will include the development of offshore wind turbines – the first of its kind in Southeast Asia. A recent study by Ember shows how offshore wind energy transmitted through subsea cables can transform subnational economies by creating industrial hubs, engineering laboratories and jobs.

One key advantage of subsea cables is that they are designed as part of a renewable energy ecosystem, rather than an extension of fossil fuel–based systems. (Chart: ASEAN Centre for Energy)

Despite opportunities, the novelty of subsea cables in the region also creates challenges. Two of the most critical issues impeding these projects are: 1) regulatory gaps; and 2) supply chains and logistics of subsea cables.

Countries involved in subsea cable projects have diverse energy markets, protocols and permitting requirements, which can impede investment and timely completion. Subsea cable projects will require Southeast Asian countries to collaborate closely on technical issues, such as the material, configuration and design of cables, legal issues such as the implications of the United Nations Convention on the Law of the Sea (UNCLOs) and governance issues, such as coordination of repair and maintenance activities and data transparency. While the Submarine Power Cable Development Framework will be useful towards providing regional guidelines, project-level implementation will require high levels of regulatory harmonization. Regulatory mechanisms, such as emergency protocols, dispute resolution mechanisms and market guidelines are urgently required to enhance investor confidence and accelerate project implementation.

Subsea power cable projects are also impeded by supply chain constraints and complex logistics. These infrastructures are in huge demand and are manufactured by a handful of companies. A recent study by the ASEAN Centre for Energy (ACE) predicts a waiting period of 10-12 years for subsea cables and converters, which can cause significant delays for the completion of the APG. Southeast Asia’s leaders need to discuss pathways for developing resilient supply chains of subsea cables and associated technologies.

An associated challenge is logistics - most manufacturers are based in Europe, which makes the transferring of cables and converters to Southeast Asia using specialized vehicles difficult and expensive. Research on subsea cables show that addressing the logistical challenges of subsea cable projects will require coordinated planning on a combination of various transport and installation options, which can include Cable Lay Vessels (CLV), cargo barges and Heay Lift Vessels (HLV).

Despite some constraints, the opportunities offered by subsea cables far outweigh the challenges. These projects can act as catalysts to increase the number of participants in energy trade, while spurring the development of green industrialization in areas with limited economic opportunities. Collaboration on the two priorities of transnational regulation and resilient supply chains can accelerate the implementation of Southeast Asia’s subsea cable projects.

[1] The Lao PDR-Thailand-Malaysia-Singapore Power Integration Project (LTMS-PIP), the region’s first multilateral power project was commissioned in 2022. See Huda et al. (2023). Accelerating the ASEAN Power Grid 2.0: Lessons from the Lao PDR-Thailand Malaysia-Singapore Power Integration Project (LTMS-PIP) (Singapore: ISEAS - Yusof Ishak Institute, 2023).

[2] Compiled by the author from various sources.

This article is a guest contribution from Mirza Sadaqat Huda. The opinions expressed are those of the author(s) and do not necessarily reflect the views of RECCESSARY.

Have insights on energy or carbon issues? Share your perspective with us! Send your submission to reccessary@gmail.com for a chance to be featured. Submissions may be edited for clarity and style.

Read more: Rewiring Asia: How global and ASEAN grids inform Taiwan’s next move