The “Asia-Pacific Carbon Markets Outlook 2025–2026” webinar, hosted by RECCESSARY, examined how carbon markets across the region are entering a new phase of implementation. (Photo: Wendy Lo)

Carbon markets across Asia-Pacific are moving into a new phase of institutionalization, where pricing, eligibility, and cross-border alignment are becoming material considerations for companies operating in the region. While governments continue to experiment with different policy designs, buyers are increasingly focused on credit quality over volume.

These dynamics were explored at a webinar titled “Asia-Pacific Carbon Markets Outlook 2025–2026,” hosted by RECCESSARY on Jan. 28. The event brought together market analysts, verification bodies, carbon traders, and academics to assess how regional carbon markets are evolving.

“The question is no longer whether international carbon markets will matter,” said Jason Huang, CEO of RECCESSARY. “The real question now is how they will shape access, participation, and competitiveness over the next few years.”

Southeast Asia moves from policy design to implementation

Across Southeast Asia, carbon pricing mechanisms are expanding rapidly, but pricing levels and compliance structures remain fragmented, according to Sherry Hu, carbon market analyst at RECCESSARY.

Hu pointed to the USD 20 per tonne threshold as an increasingly important benchmark separating emerging carbon markets from more mature ones. What makes 2026 a pivotal year for Asia, she said, is Singapore’s planned 80% carbon tax increase to SGD 45 (about 35 USD) per tonne in 2026, which will push its price above that threshold and make it the first Asian jurisdiction to do so.

“This sends a strong regional signal that carbon pricing in Asia is entering a new phase,” Hu said, adding that companies will need to pay closer attention to how compliance obligations and cost exposures differ across markets.

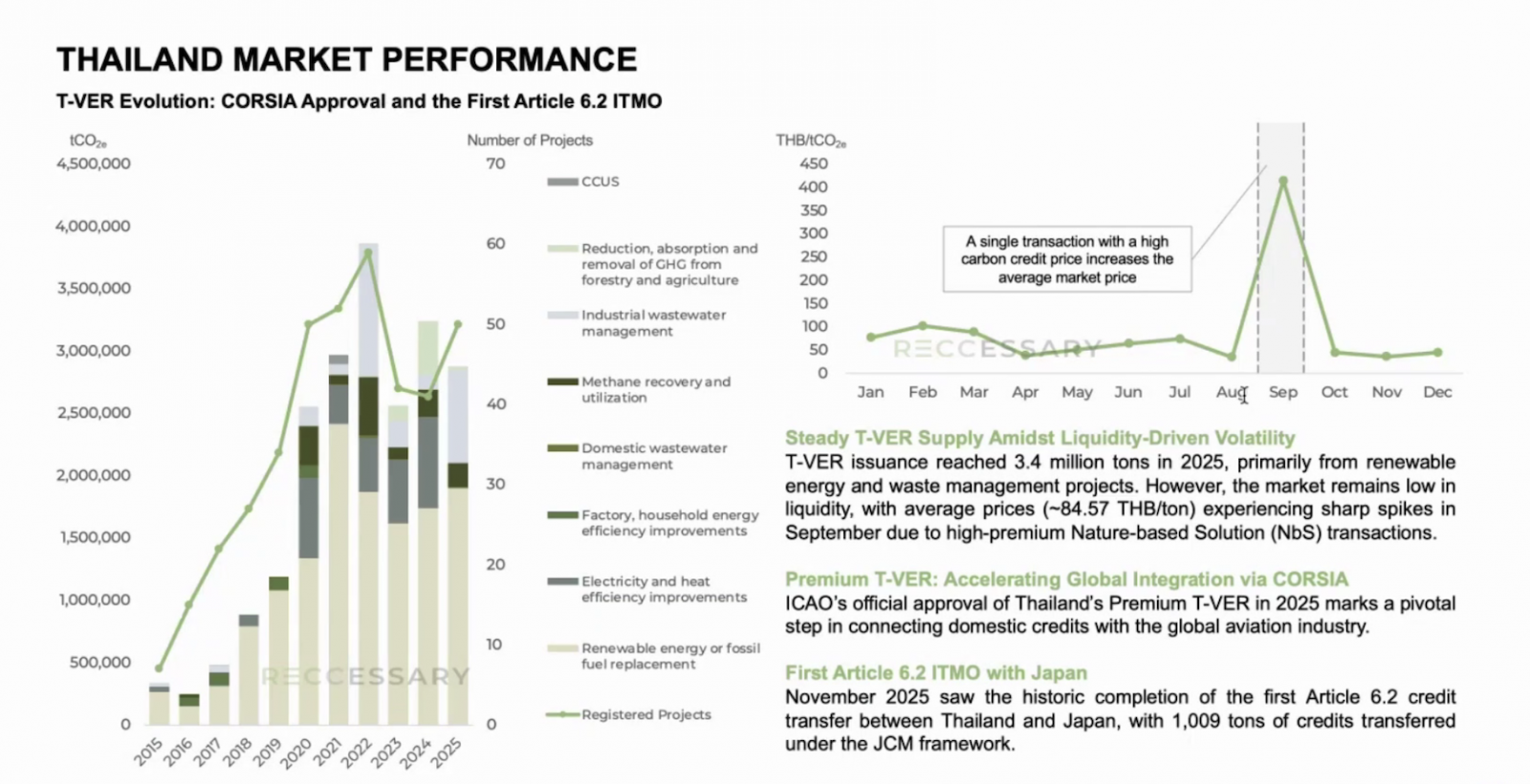

Southeast Asia also offers a glimpse into how domestic carbon markets may begin to connect with international frameworks. Thailand, Hu noted, approved its Climate Change Act in December 2025, formally anchoring both a carbon tax and the Thailand Emissions Trading Scheme (ETS) under a single legal framework.

Hu said that two developments in Thailand stand out. First, the International Civil Aviation Organization (ICAO)’s approval of premium T-VER credits for use under CORSIA in 2025 linked Thailand’s domestic credits to global aviation demand. Second, the completion of the first Article 6.2 internationally transferred mitigation outcome (ITMO) transaction between Thailand and Japan marked a step toward cross-border credit integration.

Sherry Hu of RECCESSARY highlighted two milestones in Thailand’s carbon market integration: ICAO approval of premium T-VER credits under CORSIA and the country’s first Article 6.2 ITMO transfer with Japan. (Screenshot from webinar)

Vietnam, meanwhile, launched its pilot ETS in the second half of 2025, focusing on simulated quota allocation and trading. Once legally binding quotas are introduced, Hu said, 2026 is likely to see the first significant wave of demand for carbon management, auditing, and compliance services in the country.

Why quality is now the market driver

As policy frameworks mature, attention is shifting toward carbon credit quality, according to Zach Wu, sustainability and carbon strategy lead at Welhunt Materials Enterprise.

“Quality is no longer defined by a single checklist,” Wu said. Instead, it reflects how multiple layers interact, from whether a credit can exist under registry methodologies, to whether it meets high-integrity supply standards, to whether it can be credibly used.

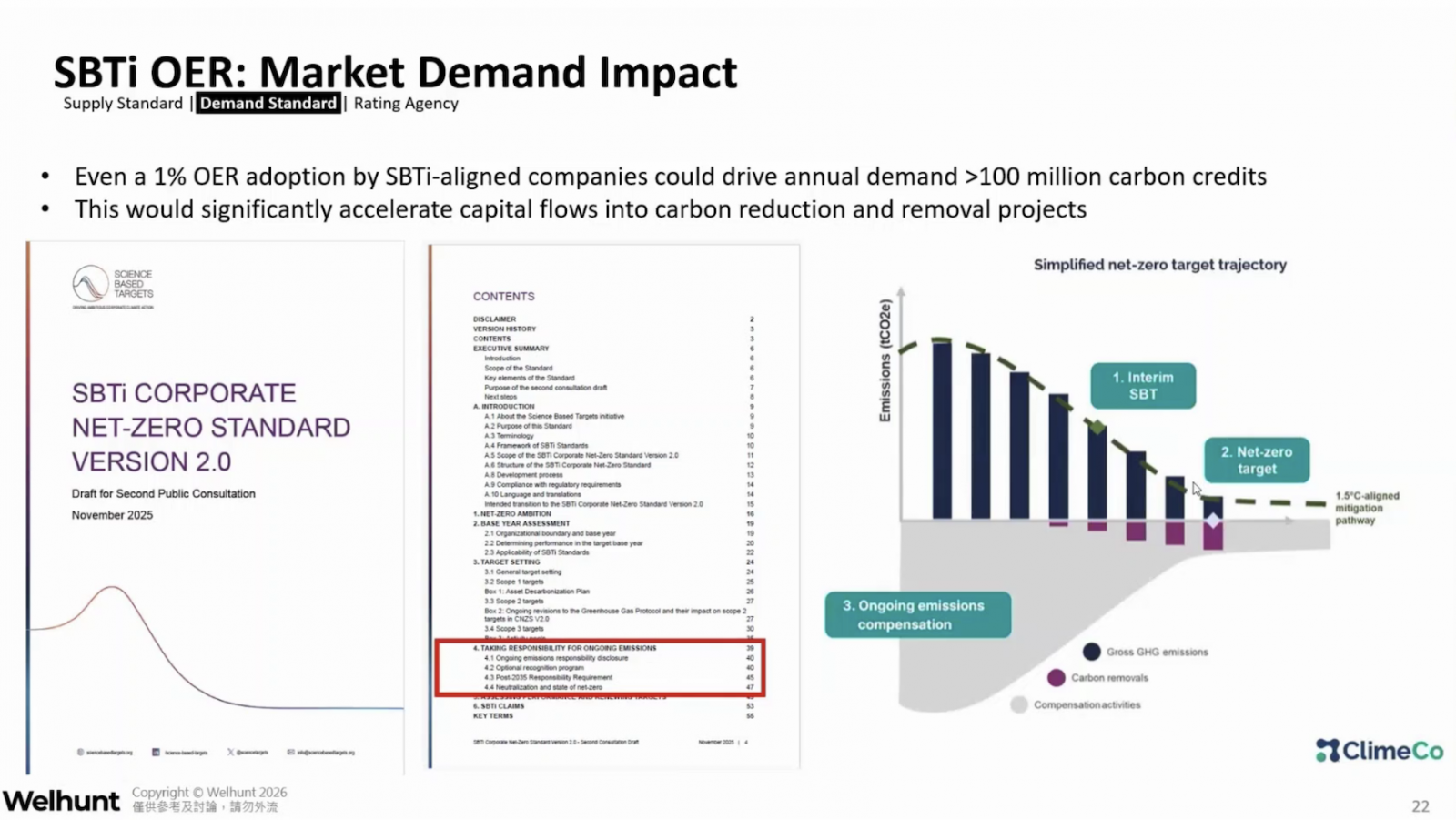

Wu highlighted the growing influence of standards such as the Science Based Targets initiative’s (SBTi) emerging Ongoing Emissions Responsibility (OER) framework. While carbon credits still do not count toward net-zero target achievement under SBTi, OER formally recognizes voluntary credit use outside target progress and signals a long-term shift toward carbon removals.

From a market perspective, Wu said, even conservative adoption could have significant implications. A 1% uptake of OER among SBTi-aligned companies could generate annual demand exceeding 100 million carbon credits, creating stable demand not tied to compliance obligations.

Zach Wu of Welhunt said even limited adoption of SBTi’s Ongoing Emissions Responsibility could generate demand for more than 100 million carbon credits annually. (Screenshot from webinar)

“From a trader's perspective, the biggest change we see globally is a clear shift from quantity to quality,” Wu said.

According to Sylvera’s State of Carbon Credits 2025 report, total retirements fell 4.5% last year, but market value rose 6% to USD 1.04 billion, as buyers paid more for higher-quality credits.

Taiwan faces structural constraints as carbon pricing takes effect

Taiwan enters 2026 with a new carbon fee system in force, introducing a distinct compliance logic for domestic industries, Hu said. The system sets a standard rate of NTD 300 (USD 9.59) per tonne, with preferential rates available for companies that meet reduction targets, particularly in sectors facing high carbon leakage risk.

Despite policy progress, Taiwan’s carbon credit market continues to face structural challenges, Hu said. Trading volumes remain low due to limited liquidity, supply shortages, and a wide price gap between domestic credits and the carbon fee. Although project registrations doubled year-on-year in 2025, supply is heavily concentrated in energy efficiency projects, reflecting a preference for mature methodologies.

These constraints are also evident in the development of nature-based credits. While Taiwan’s forests represent a significant carbon sink, with the potential to remove up to 21.9 million metric tonnes of CO₂ annually, translating that capacity into credible and scalable carbon credits will depend on the development of robust methodologies, long-term monitoring systems, and sufficient verification capacity, said Jack Lu, senior technical manager at ARES International Certification.

How Article 6 is shaping the Asia-Pacific carbon market

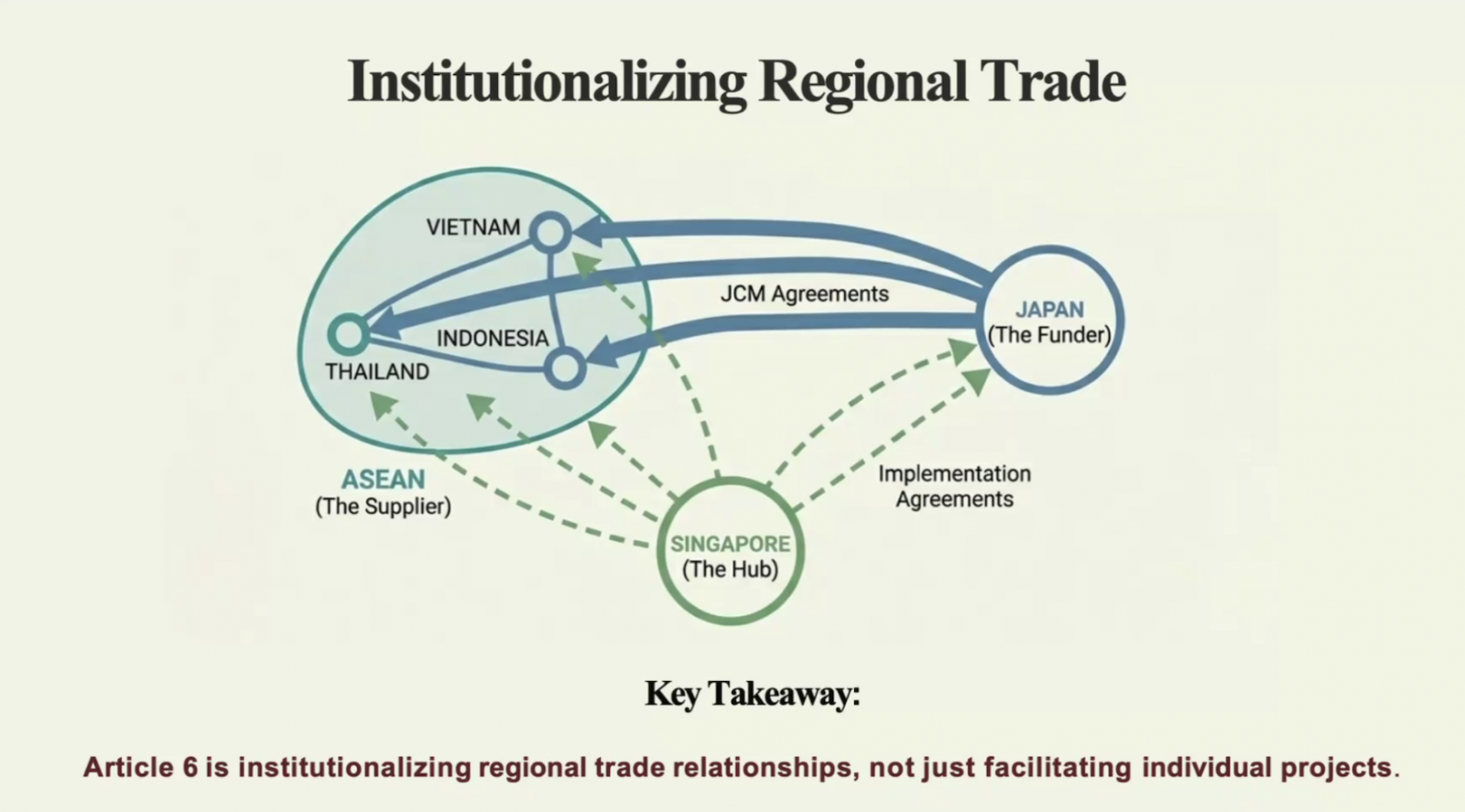

Beyond near-term market frictions, Chien-Te Fan, professor at National Tsing Hua University, framed Taiwan’s challenges within a broader regional realignment driven by Article 6. Rather than reshaping carbon markets solely through individual credit transactions, Fan said Article 6 is institutionalizing how countries trade, cooperate, and compete in the low-carbon economy.

In Asia-Pacific, this emerging carbon market structure is already taking shape. Japan has positioned itself as a primary funder through bilateral mechanisms such as the Joint Crediting Mechanism (JCM), while Singapore is increasingly defining its role as a regional hub via implementation agreements and Article 6-aligned transactions. Other economies in the region, Fan noted, are gradually being integrated as suppliers within this evolving ecosystem.

However, Taiwan occupies a unique position. As a non-party to the UNFCCC, it lacks formal authorization to participate in Article 6 transactions, yet remains deeply embedded in global supply chains and exposed to external carbon constraints such as the EU’s carbon border adjustment mechanism (CBAM). “Taiwan cannot opt out of Article 6 impacts,” Fan said, even without formal participation.

Fan argued that Taiwan’s response should focus first on building Article 6 readiness at home, by aligning domestic MRV systems, registries, and standards with international requirements. At the same time, Taiwan can leverage the agility of its private sector, with companies acting as investors, technology providers such as digital MRV solutions, or buyers of Article 6-aligned credits abroad. In this model, Taiwan could position itself as a provider of high-tech decarbonization solutions and digital infrastructure for regional carbon markets, Fan noted.

Chien-Te Fan of National Tsing Hua University said a regional carbon market architecture is taking shape, with Japan as a key funder, Singapore as a hub, and other economies positioned as credit suppliers, while Taiwan could play a role as a provider of decarbonization technologies. (Screenshot from webinar)

As carbon markets across Asia-Pacific evolve, speakers emphasized that companies should focus less on short-term price signals and more on long-term positioning.

Companies that secure verification resources early and build diversified portfolios of high-integrity assets, Hu said, are likely to be better positioned as carbon markets tighten and scarcity becomes more pronounced in the years ahead.

RECCESSARY will release the Global Carbon Market Trends: 2025 Recap & 2026 Outlook report on Feb. 26, offering a comprehensive review of global carbon market developments and forward-looking insights. Stay tuned for more.