(1).jpg)

Thai auto parts suppliers face rising pressure to retool for EV production while investing in renewable electricity, energy efficiency and carbon management. (Photo: iStock)

RECCESSARY will host an in-person, closed-door seminar in Bangkok, Thailand on July 2, titled “Green Resilience: Global Decarbonization Competition & Strategic Positioning in Thailand’s Supply Chain.”

The seminar will bring together corporate buyers, Thai industry associations, analysts, and solution providers to examine real-world cases and translate decarbonization targets into actionable pathways. Register Now.

Thailand’s auto parts industry is facing a transition that is both technological and environmental, with each pressure reshaping what it means to remain competitive as a supplier.

The technological shift is already visible in the customer base. The Japanese OEMs that anchored Thailand’s auto supply chain for decades are reducing capacity, while Chinese EV manufacturers are building local production under the EV3 and EV3.5 incentive schemes.

At the same time, automakers are pushing greenhouse gas disclosure and reduction requirements deeper into their supplier networks, and the EU’s Carbon Border Adjustment Mechanism (CBAM) is beginning to raise the cost of carbon-intensive materials such as steel and aluminum.

For Thai suppliers, these pressures are arriving together. Retooling for EV components requires new equipment, production processes and technical capabilities, while decarbonization requires investment in renewable electricity, energy efficiency, carbon accounting and supplier engagement. Both demands are emerging as vehicle production slows and margins come under pressure.

“The automotive industry is entering a new phase where competitiveness is increasingly shaped by sustainability,” Sutheep Ratnabhas, President, Asia at Maxion Wheels and Vice President of the Electric Vehicle Association of Thailand (EVAT), said in written responses to RECCESSARY. He said quality, cost and delivery remain fundamental, but OEMs are increasingly evaluating manufacturers' energy sourcing and emissions reduction efforts alongside traditional supplier metrics.

OEM pressure moves beyond quality and cost

For most of the past three decades, Thailand’s auto parts sector was shaped by Japanese OEM requirements: precision, reliability, cost control and just-in-time delivery. Carbon performance was not absent from supplier discussions, but for many companies it remained closer to a reporting issue than a procurement condition.

That balance is shifting as Thailand’s traditional customer base contracts and new EV manufacturers enter the market. Vehicle production in Thailand fell by roughly 20% in 2024 to around 1.5 million units, with the downturn continuing into early 2025. Several Japanese automakers have reduced or closed production capacity in the country, including Subaru, Suzuki, Honda and Nissan.

At the same time, Chinese EV manufacturers including BYD, Changan, Great Wall Motor, and GAC Aion are expanding local production. More than THB 137 billion (USD 4.1 billion) has been committed under Thailand’s EV incentive schemes.

But the shift from internal combustion engine vehicles to EVs is not a one-for-one replacement for local suppliers. EV platforms require different components, different production capabilities, and different supplier qualification standards. Increasingly, carbon disclosure is becoming part of the qualification process.

Bain & Company research found that leading automotive OEMs have reduced upstream Scope 3 emissions by only 2% since 2017, while Tier 1 suppliers’ upstream Scope 3 emissions increased by 5% over the same period. As OEMs try to close that gap, they are pushing emissions measurement and reduction requirements into their supplier base.

Sutheep said Maxion has seen customer expectations change clearly over the past two years, with environmental performance increasingly assessed alongside traditional supplier metrics.

“OEMs are asking suppliers to demonstrate credible carbon reduction plans, greater transparency around emissions and increased use of renewable energy,” he said.

Somboon Advance Technology (SAT), one of Thailand’s largest listed auto parts manufacturers, made a similar point in its 2025 sustainability report, saying automotive customers had requested cooperation on greenhouse gas data collection and short- and long-term emissions reduction targets.

Krungsri Research, in written responses to RECCESSARY, said international OEMs are the main channel through which these requirements are being transmitted. European and Japanese customers currently apply the most demanding standards, while Chinese EV OEMs are still at an earlier stage. However, Chinese manufacturers are also operating in a global regulatory environment shaped by carbon markets, EU supply chain rules, and SBTi-linked customer expectations.

The pressure is also segment-specific. Tire manufacturers face an additional compliance burden through the EU Deforestation Regulation, which requires deforestation-free natural rubber traceability for tire exports to Europe. For Thailand, one of the world’s largest natural rubber producers, that requirement is already directly relevant.

Listed suppliers show the dual transition in real time

The overlap between EV retooling and decarbonization is already visible in the sustainability disclosures of Thailand’s major listed auto parts manufacturers.

Somboon Advance Technology produces axle shafts, disc brakes, and hub wheels, with core exposure to pickup truck components and agricultural machinery parts. These are among the segments most affected by Thailand’s production slowdown. In 2025, Thailand’s total vehicle production was around 1.43 million units, down 2%, while agricultural machinery production fell 15%, according to Somboon Advance Technology’s 2025 sustainability report.

Against that weaker production backdrop, SAT reported a 35% absolute reduction in Scope 1 and 2 greenhouse gas emissions in 2025 compared with its 2018 baseline, surpassing its 2030 target of a 30% reduction ahead of schedule.

Because part of the reduction came from lower production volumes, the company’s emissions intensity performance is a more useful indicator of structural improvement. SAT’s emissions intensity per unit of production fell 24.7%, compared with a 17% target.

SAT has also started building upstream carbon management capacity. In 2025, the company organized a supplier training program on greenhouse gas inventory preparation for 27 suppliers and 53 participants, with plans to provide on-site advisory services in 2026.

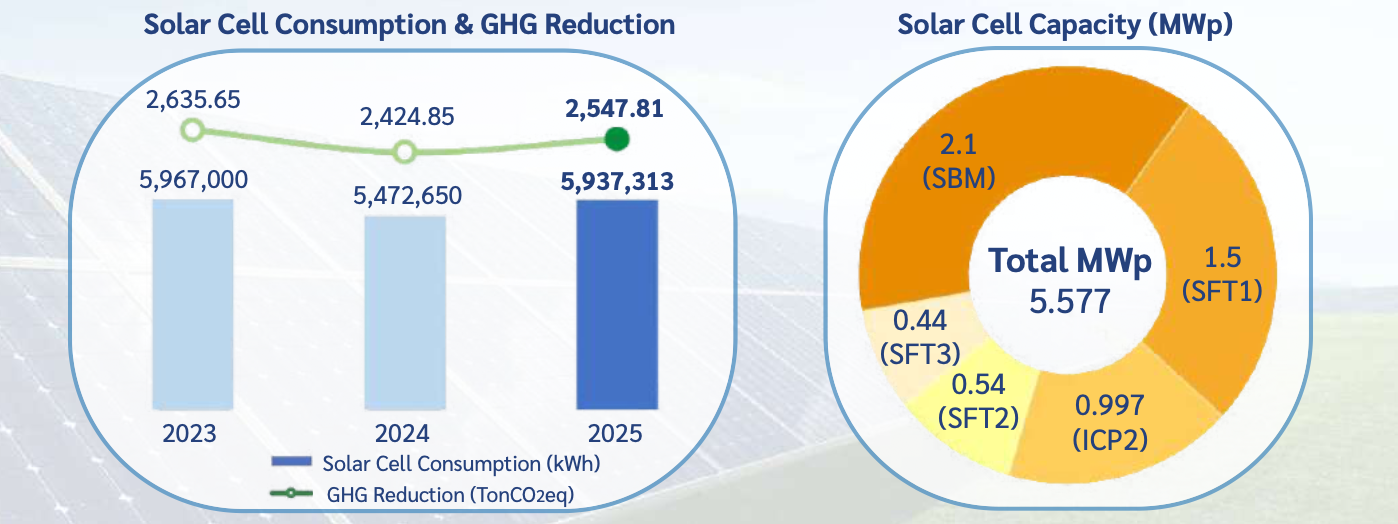

However, SAT’s renewable electricity use remains more limited. The company sourced 4.74% of its electricity from rooftop solar systems across five facilities, supported by 5.58 MWp of installed capacity. Its 2030 renewable electricity target is 10%.

Somboon Advance Technology’s solar power capacity reached 5.577 MWp in 2025, supplying 5.94 million kWh of electricity and reducing emissions by about 2,548 tCO₂e. (Source: Somboon Advance Technology sustainability report 2025)

AAPICO Hitech offers a second example of how supplier transition is being shaped by both customer change and decarbonization pressure. The company supplies metal forming, chassis, structural, and plastic parts to customers including Ford, Mitsubishi, MG, and Changan. Its relationship with Changan places it directly within the shift from Japanese ICE supply chains to Chinese EV supply chains.

AAPICO has set a carbon neutrality target for 2048, with interim goals to cut Scope 1 and 2 emissions by 50% by 2030 and 70% by 2038. Its electricity consumption fell 10.28% in 2024, from 65,179 MWh to 58,478 MWh. At its Rayong facilities, 17.78% of electricity came from rooftop solar, while AAPICO is expanding solar deployment across its broader facility network.

Maxion Wheels’ Saraburi plant in Thailand was Maxion’s first aluminum wheel plant globally to adopt on-site solar generation, beginning with a 1.6 MW rooftop solar installation commissioned in January 2022. A 3.06 MW ground-mounted solar installation followed in January 2024, bringing total renewable capacity at the plant to 4.66 MW.

Maxion Wheels’ Saraburi plant in Thailand has 4.66 MW of on-site solar capacity, making it the company’s first aluminum wheel facility globally to adopt solar generation. (Photo: Maxion Wheels)

Based on current production of approximately 1.2 million wheels a year, the projects supply around 25% of the Saraburi plant’s electricity consumption and reduce emissions by around 3,100 tonnes of CO₂ annually, according to Sutheep.

“The experience reinforced that successful decarbonization requires engineering, operations, finance and business strategy to work together,” Sutheep said.

CBAM adds a cost dimension to supplier decarbonization

While OEM requirements create a market access risk, CBAM is turning embedded carbon into a more direct cost issue for manufacturers that depend on steel and aluminum.

From Jan. 1, 2026, EU importers must purchase and surrender CBAM certificates based on the embedded emissions of covered goods. The first phase covers iron and steel, aluminum, cement, fertilizers, electricity, and hydrogen.

Auto parts are not yet directly covered, but Thai parts manufacturers are exposed through their material inputs. A typical one-tonne vehicle contains around 600 kilograms of steel and 90 kilograms of aluminum. As steel and aluminum producers pass through CBAM-related costs, downstream parts manufacturers are likely to face higher input prices.

The larger risk is the proposed downstream expansion. A European Commission proposal in December 2025 would bring around 180 downstream products into CBAM scope by January 2028, including automotive components such as wheels, gearboxes, and certain engines.

For Thai auto parts exporters, that creates a two-year adjustment window. Manufacturers using fossil-heavy grid electricity and carbon-intensive steel or aluminum could face higher compliance costs than competitors in markets with cleaner power systems or lower-carbon material supply. That risk is especially relevant for aluminum-intensive segments such as wheels.

Sutheep said decarbonization should not be viewed only as an additional cost, because many emissions reduction measures also improve operational efficiency and resilience.

“Companies that move early are likely to build stronger customer relationships and create long-term competitive advantage,” he said. “Sustainability and competitiveness should reinforce one another.”

Renewable power access remains the structural gap

Thai manufacturers can improve energy efficiency, install rooftop solar where space and load profiles allow, and begin measuring supplier emissions. But large-scale access to verifiable renewable electricity remains limited.

Maxion’s comparison between Thailand and India shows why procurement models matter. In Thailand, the Saraburi plant has relied on on-site renewable generation. In India, Maxion’s three manufacturing plants in Pune have invested in dedicated off-site solar parks since November 2023, with renewable electricity generated remotely and credited to the facilities through the national grid. The company has also expanded into wind energy, with procurement beginning in December 2025 at two plants and June 2026 at the third.

Across the three Indian plants, Maxion has approximately 16.8 MW of solar capacity and 2.85 MW of wind capacity. Depending on the facility, renewable energy now supplies around 40% to 55% of electricity demand.

The contrast shows how different regulatory frameworks shape the speed and scale of industrial decarbonization. Thailand’s on-site solar model can deliver meaningful emissions reductions at individual facilities, but off-site procurement mechanisms can allow manufacturers to reach a much higher renewable electricity share where regulation and grid structures support it.

Sutheep said the procurement models and technologies may vary by country, but the underlying objective remains the same, which is to reduce emissions while keeping manufacturing reliable and cost-competitive.

From EVAT’s perspective, Sutheep said Thailand’s ability to maintain its position as one of Southeast Asia’s strongest automotive manufacturing ecosystems will depend on expanding access to renewable electricity, strengthening supplier capabilities in carbon management, encouraging continued investment in advanced manufacturing, and maintaining stable long-term industrial policies.

“The future of automotive manufacturing will increasingly depend on a manufacturer’s ability to reduce emissions, secure renewable energy and provide transparent carbon reporting,” he said.