.jpg)

Thailand’s PCB boom has attracted more than THB 200 billion in investment since 2022, but renewable electricity access remains a key constraint. (Photo: Pixabay)

RECCESSARY will host an in-person, closed-door seminar in Bangkok, Thailand on July 2, titled “Green Resilience: Global Decarbonization Competition & Strategic Positioning in Thailand's Supply Chain.”

The seminar will bring together corporate buyers, Thai industry associations, analysts, and solution providers to examine real-world cases and translate decarbonization targets into actionable pathways. Register Now.

Thailand has become ASEAN’s largest PCB production base, attracting more than THB 200 billion (USD 6.1 billion) in investment across 180 projects since 2022. As global electronics companies place greater emphasis on supply chain decarbonization, access to renewable electricity is becoming an increasingly important factor in sustaining the country's competitive advantage.

The investment boom has been driven by supply chain diversification and rising demand for AI servers, electric vehicles, and advanced electronics, drawing Taiwanese, Chinese, and Japanese manufacturers to expand production in Thailand. Yet securing renewable electricity is proving more difficult than attracting new investment.

PCB manufacturers are responding by investing in rooftop solar, measuring product carbon footprints, and exploring renewable energy certificates. However, renewable electricity still accounts for only around 3% of power consumption at some of Thailand's leading producers.

Decarbonization requirements are moving deeper into the supply chain

For global technology companies, renewable energy and emissions management are no longer corporate aspirations but procurement requirements. The Global Electronics Association and the Responsible Business Alliance have jointly issued guidance on Scope 3 emissions from purchased goods and services specifically for the electronics sector, signaling that suppliers beyond the first tier will increasingly come under scrutiny.

The pressure is already reaching Thai manufacturers, though unevenly across end markets. In written responses to RECCESSARY, Krungsri Research said automotive and medical applications are moving fastest because competition in these segments depends increasingly on quality, reliability, and compliance rather than price.

In particular, EV manufacturers and European and Japanese customers are increasingly treating carbon reporting, low-carbon sourcing, and supply chain transparency as prerequisites for remaining in the supply chain.

Telecom, computer components, and electrical appliance customers are also raising sustainability expectations, even though cost remains the dominant purchasing criterion and has slowed the adoption of decarbonization requirements.

Over the next three to five years, Krungsri Research expects decarbonization to evolve from a differentiator into a qualifying requirement, joining cost, technology, and scale as a baseline condition for competing in higher-value supply chains.

PCB manufacturers struggle to close the renewable electricity gap

Thailand’s largest PCB manufacturers have begun implementing decarbonization measures, though progress remains modest.

KCE Electronics, a Thai-owned and Thai-listed manufacturer, reduced Scope 1 and 2 emissions by 18.8% in 2025 compared with its 2022 baseline, surpassing its interim target of an 11% reduction. Much of the improvement came from energy efficiency measures, including upgrades to production cooling systems.

KCE Electronics upgraded its production cooling systems to improve energy efficiency, generating THB 10.5 million in electricity cost savings and reducing greenhouse gas emissions by 1,170 tCO₂e. (Photo: KCE Sustainability Report 2025)

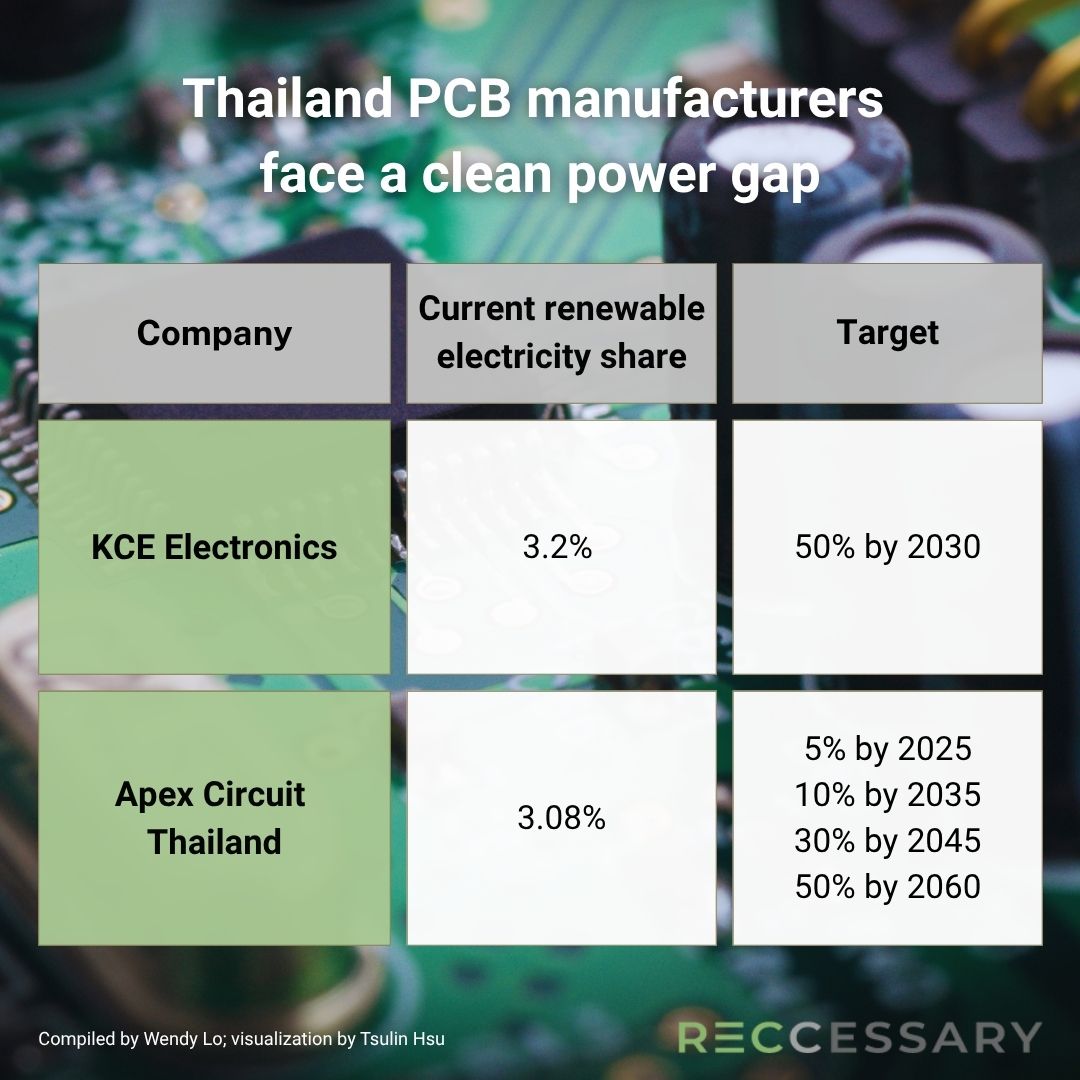

Yet renewable electricity remains limited. KCE targets a 50% share of renewable energy by 2030, but renewables accounted for just 3.2% of total electricity consumption in 2025. The entire amount came from a 3.5 MW rooftop solar system generating approximately 4,500 MWh annually.

The company is studying additional renewable procurement options, including power purchase agreements, and is monitoring policy developments. It also plans to procure I-RECs and has begun developing product carbon footprint programs under ISO 14067.

Apex International, a Taiwan-invested manufacturer with Thailand-based operations through Apex Circuit Thailand, presents a sharper version of the same gap. Renewable energy accounted for 3.08% of total energy consumption, generated entirely from on-site solar installations. Apex plans to expand its solar capacity to around 21 MWp by 2028 and signed an SBTi commitment in 2024.

However, the company has yet to establish formal science-based targets, and its own climate risk disclosures identify customer demands for carbon reduction strategies and evidence of carbon neutrality as an emerging business risk.

In May 2025, Apex Circuit Thailand signed a Power Purchase Agreement with renewable energy developer Constant Energy covering both an on-site solar installation and an off-site solar project structured under Thailand’s emerging Third-Party Access (TPA) framework. If implemented, the arrangement would make Apex one of the first PCB manufacturers in Thailand to procure renewable electricity from an off-site source through the grid, moving beyond self-generation toward the type of verifiable renewable supply increasingly sought by global customers.

Power market remains the industry’s biggest constraint

The gap between customer expectations and corporate progress is not primarily the result of insufficient ambition. It reflects the structure of Thailand’s electricity market.

Thailand has historically operated under a single-buyer model, with the Electricity Generating Authority of Thailand (EGAT) serving as the sole wholesale purchaser of electricity. For industrial users, renewable procurement options have largely been limited to self-generation and renewable energy certificates.

The government has begun introducing alternatives. Utility Green Tariff (UGT1), launched in early 2025, and UGT2, introduced in March 2026, allow businesses to purchase electricity bundled with renewable energy certificates. But these programs differ fundamentally from the direct procurement arrangements increasingly sought by multinational corporations and RE100 participants.

Thailand’s direct power purchase agreement (DPPA) pilot represents a more significant reform because it would allow eligible users to contract directly with renewable generators through third-party grid access. Yet the pilot remains restricted to data centers. PCB manufacturers are excluded.

The Federation of Thai Industries has called for Direct Power Purchase Agreement (DPPA) implementation for manufacturers by 2026, arguing that access to renewable electricity has become a competitiveness issue rather than merely an environmental objective.

The Energy Regulatory Commission (ERC) said in March that the DPPA scheme could eventually be extended to industries such as PCB manufacturing, electronics, and electric vehicles in the coming years.

The options currently available to PCB manufacturers therefore remain limited to expanding rooftop solar installations, purchasing renewable energy certificates, and waiting for broader market reforms.

Clean power becomes Thailand’s next PCB growth barrier

The decarbonization challenge is arriving at the same time as a wave of foreign-invested PCB capacity entering Thailand. More than THB 200 billion in BOI-approved investment since 2022 has intensified competition in segments where Thai manufacturers already face margin pressure.

Krungsri Research noted that Thailand’s five largest PCB manufacturers maintained average net profit margins of around 4.2% between 2021 and 2023, while smaller manufacturers posted losses. Meanwhile, many foreign entrants like Zhen Ding Tech and Unimicron are arriving with sustainability frameworks already developed under the pressure of global technology OEMs.

For Thai-owned manufacturers, this creates dual pressure from intensifying cost competition and rising decarbonization requirements.

Traditional competitive factors such as cost, technology, and scale will remain decisive. But access to renewable electricity is increasingly becoming a prerequisite for participation in higher-value global supply chains.

For investors, the outlook suggests that the constraint could ease over time. Thailand is expanding green electricity offerings through UGT2, developing third-party access rules, and considering a broader expansion of the DPPA framework beyond data centers.

The forthcoming Climate Change Act and the revised Power Development Plan, which targets a 60% clean electricity share by 2050, also point toward a more supportive policy environment.

Thailand built its position as ASEAN’s largest PCB production base on cost, infrastructure, and policy stability. Holding that position in the next phase will depend on something the country has not yet delivered at scale: affordable, verifiable renewable electricity for manufacturers.