.jpg)

Vietnam may overtake Thailand in nominal GDP in 2026. But does the ranking tell the full story? (Photo: iStock)

Vietnam recorded 8.02% GDP growth in 2025, GDP at current prices reached USD 514 billion, placing it among the fastest-growing economies globally. According to Nikkei Asia, the country is on course to overtake Thailand in nominal GDP as early as this year, potentially becoming Southeast Asia’s third-largest economy.

Thailand’s macroeconomic picture is, by contrast, more subdued. The Organization for Economic Co-operation and Development (OECD) forecasts Thailand’s real GDP growth at around 1.5% in 2026, lagging most ASEAN peers.

Yet headline comparisons only tell part of the story. “Vietnam is unlikely to surpass Thailand this year,” said Kristy Hsu (徐遵慈), Director at the Taiwan ASEAN Studies Center of the Chung-Hua Institution of Economic Research.

Kristy Hsu, Director at the Taiwan ASEAN Studies Center of the Chung-Hua Institution of Economic Research, discusses how risk profiles are diverging between Vietnam and Thailand as the year unfolds. (Photo: Wendy Lo)

Based on International Monetary Fund data, Vietnam would still not overtake Thailand by 2026, even under a scenario where Vietnam sustains 10% growth while Thailand grows at around 2%. A lead in 2026, she added, would not necessarily be permanent, as the ranking could shift again the following year. GDP rankings, Hsu cautioned, remain fluid and sensitive to external factors such as currency movements, and short-term changes in nominal GDP should not be treated as a standalone measure of competitiveness.

From an investor perspective, Hsu said, the comparison should not be framed as a binary choice between Vietnam and Thailand. The two economies play fundamentally different roles within regional supply chains, meaning investors targeting Vietnam typically do not view Thailand as a direct substitute, and vice versa. Instead, the more relevant question lies in how risk profiles differ across the two markets as the year unfolds.

Politics set the tone for economic direction

The start of the year in both countries has been shaped by major political milestones. On Jan. 23, Vietnam concluded its 14th National Party Congress, the Communist Party’s once-every-five-years convention, which laid out ambitious economic targets for the next planning cycle. Prime Minister Pham Minh Chinh had earlier announced a target annual growth rate of 10% for 2026 in December 2025. At the congress, General Secretary To Lam further set an objective of maintaining 10% annual GDP growth between 2026 and 2030.

In Vietnam’s political system, Hsu noted, economic targets set at the party level carry significant weight, shaping policy priorities and implementation across the government. Vietnam’s growth has been closely tied to a state-led infrastructure push and rising public investment. Public investment for 2026 is expected to increase by around 26%, which could add roughly 1.6 percentage points to economic growth.

In Thailand, the democratic system is entering a more uncertain phase, with a general election scheduled for February. According to polling results as of Jan. 27, the current ruling party is unlikely to secure a majority, raising questions about policy continuity. New initiatives drafted toward the end of 2025 or expected to roll out in 2026 remain subject to political negotiation.

Still, Hsu stressed that political uncertainty has not translated into an investor exodus. “Have you seen foreign investors collectively pulling out of Thailand? No,” she said. “Despite periodic policy adjustments, Thailand’s overall policy direction has remained supportive of foreign investment, and that is unlikely to change.”

That support is anchored in Thailand’s Board of Investment (BOI) framework, which emphasizes targeted incentives rather than across-the-board tax relief. BOI-promoted projects in targeted sectors such as advanced manufacturing, electronics, electric vehicles (EVs), and semiconductors can receive corporate income tax exemptions of up to eight years, extendable to as long as 13 years for projects classified as strategic. In recent years, the BOI has emphasized “quality investment,” linking incentives to technology transfer, local value creation, and human capital development rather than investment size alone.

Vietnam, by contrast, relies more heavily on tax-based incentives as a core investment attraction tool. Eligible projects may qualify for a preferential corporate income tax rate of 10% for up to 15 years, alongside tax holidays of up to four years and subsequent 50% tax reductions for up to nine years. These incentives are particularly targeted at manufacturing, high-tech sectors, and projects located in designated economic zones.

What investors really compare

For foreign investors, the most decisive considerations include GDP per capita, wage levels, and free trade agreements (FTAs), Hsu said. GDP per capita matters most for companies targeting domestic demand, as it reflects purchasing power. As a more mature economy, Thailand’s GDP per capita stands at USD 7,980, compared with USD 4,740 in Vietnam.

Vietnam’s edge lies instead on the cost and trade side. Lower wages continue to attract export-oriented manufacturing, while an extensive trade network, with 17 FTAs in force, provides preferential access to overseas markets. That dynamic is reflected in 2025 export data: Vietnam’s total exports reached USD 475 billion, compared with Thailand's USD 339.6 billion.

Foreign direct investment patterns, however, highlight a structural divergence rather than a simple extension of this advantage. Vietnam attracted USD 38.4 billion in FDI in 2025, up 0.5% year-on-year. Manufacturing and processing drew the largest share of newly registered capital, at US$9.8 billion, accounting for 56.5% of the total. The top three investors by value were Singapore, China, and Hong Kong.

Thailand recorded USD 43.6 billion in FDI in 2025, a 66% year-on-year increase. By investment value, the digital sector attracted the most capital, followed by electronics and metals and materials, reflecting Thailand’s more mature, higher-value investment profile. The top three investor sources were Singapore, Hong Kong, and China.

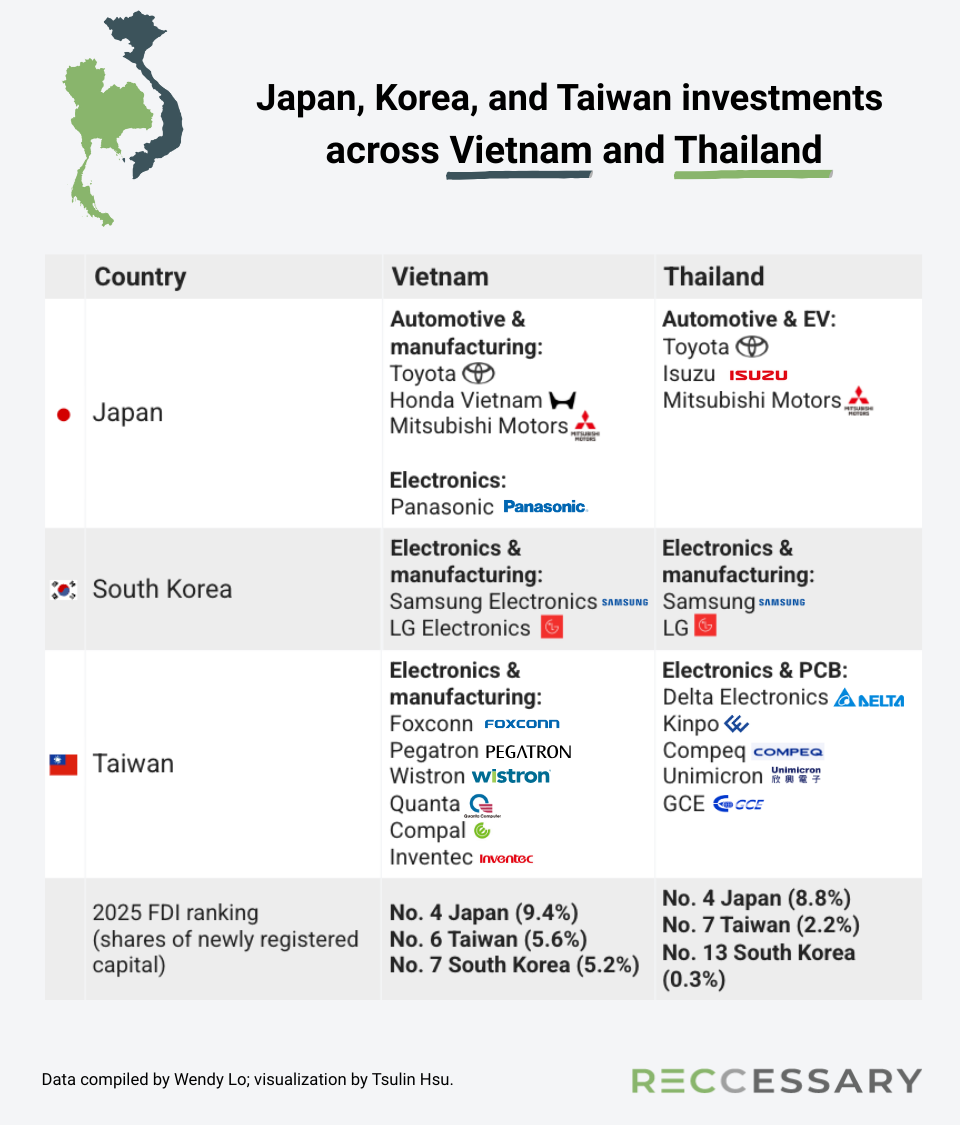

While headline FDI sources overlap, the structure and intent of investment differ. Northeast Asian capital, in particular, plays a defining role in shaping how each economy is positioned within regional supply chains. Japanese, South Korean, and Taiwanese firms are deeply embedded across manufacturing, electronics, and automotive supply chains in Vietnam and Thailand, but with different sectoral focuses and strategic objectives.

Supply chain depth further differentiates the two markets. Vietnam’s electronics sector remains concentrated in lower value-added activities, such as final assembly and processing based on imported components, with limited upstream production of key parts and materials. Thailand, by contrast, has moved further into printed circuit boards (PCBs), EVs, and other higher-value applications. Both governments are seeking to upgrade their industrial ecosystems, but through different pathways.

Vietnam aims to move beyond its midstream position by reducing dependence on imported components, offering incentives to manufacturers that expand local sourcing and production coverage. Thailand, meanwhile, is pursuing a more technology-intensive transition. Its national semiconductor strategy targets around USD 79 billion in investment by 2050.

Hsu noted that Thailand’s softer growth outlook reflects the challenges of this transition phase. The country is experiencing “growing pains” associated with industrial upgrading, she said, and policymakers must proceed carefully to avoid the risk of falling into a prolonged middle-income trap.

Investment patterns underscore these structural differences. Thailand’s manufacturing base remains substantial, particularly in automotive and electronics, but recent inflows have been more selective. Japanese automakers and component suppliers remain deeply embedded, and Japanese investment applications surged 105.7% year-on-year in the first nine months of 2025, a rise linked to the “Quick Big Win” strategy targeting future industries, including electric vehicles, semiconductors, and digital technology.

In Vietnam, an extensive network of free trade agreements has helped attract investment from South Korea and Japan, alongside sustained inflows from Taiwanese manufacturers. Vietnam now accounts for 50% of South Korea’s total trade with ASEAN, underscoring its growing role in Korean supply chains. Major Taiwanese ICT firms, including Foxconn, Quanta, and Wistron, have also established manufacturing bases across the country.

Five years after the EU–Vietnam Free Trade Agreement entered into force, bilateral trade reached USD 300 billion, further cementing Vietnam’s role as a key export platform.

Infrastructure and compliance shape investment decisions

Looking ahead, compliance capacity is emerging as a new fault line, said Sean Li (李明勳), a research analyst at the Taiwan ASEAN Studies Center. As the EU’s Carbon Border Adjustment Mechanism (CBAM) takes effect in 2026, Vietnam’s limited monitoring, reporting, and verification (MRV) systems leave it reliant on foreign firms to build emissions-tracking capabilities. Thailand, by contrast, has more established legal frameworks for ESG compliance and carbon accounting.

Infrastructure remains another differentiator. Repeated power outages disrupted Vietnam’s industrial production in recent years, with the World Bank estimating losses of USD 1.4 billion, or 0.3% of GDP, during the 2023 power crisis. Thailand retains an advantage in electricity supply stability, while Vietnam is working to catch up through power development plans and longer-term ambitions, including nuclear energy.

A longer race, not a single turning point

Longer-term projections suggest Vietnam’s GDP could reach USD 994 billion by 2035, potentially surpassing both Thailand and Singapore. Even so, Hsu cautioned against reading too much into near-term rankings. Vietnam’s recent momentum is notable, she said, but closing the gap in overall economic scale remains a multi-year process, likely requiring five to eight years or more.

Rather than a race for rankings, the comparison reflects how Vietnam and Thailand, at different stages of development, present distinct risk profiles and strategic considerations for investors in a more fragmented global trade environment.

'Vietnam vs. Thailand competitiveness' series

- Energy as a competitive lever: How Vietnam, Thailand compete for green manufacturing investment

- Energy as a competitive lever: How GreenYellow is building renewable energy solutions for manufacturers in Vietnam

- Energy as a competitive lever: WHAUP integrates green power and infrastructure for industrial growth

- Energy as a competitive lever: CCET navigates renewable opportunities and constraints in Thailand

RECCESSARY’s upcoming webinar, “Beyond ASEAN: Mastering Decarbonization Strategy in Thailand & Vietnam,” will take place on April 21.

The session will unpack net-zero regulations, CBAM readiness, green power procurement strategies, and what lies ahead for low-carbon manufacturing across Vietnam and Thailand.

Seats are limited. Register now.