.jpg)

Thailand-based industrial developer WHA Utilities and Power is positioning energy as a core part of industrial infrastructure. (Photo: WHAUP)

“The first question when companies are investing is whether there is sufficient power supply, and how much green energy we can provide,” said Akarin Prathuangsit, CEO of WHA Utilities and Power Public Company Limited (WHAUP), in an interview with RECCESSARY.

For companies evaluating new manufacturing sites in Southeast Asia, electricity is no longer just a cost consideration. Industrial developers say prospective tenants are now asking how much power can be secured, how reliable the supply is, and increasingly, how much of that electricity can come from renewable sources.

While demand for green power is rising, the reality on the ground remains constrained. Most industrial estates today can only supply around 15 to 20% of tenants’ electricity needs through on-site renewable energy. Bridging that gap, Akarin said, will require not only new policy mechanisms, but also a shift in how energy is delivered, priced and integrated within industrial infrastructure.

From land to infrastructure: competing on integrated utilities

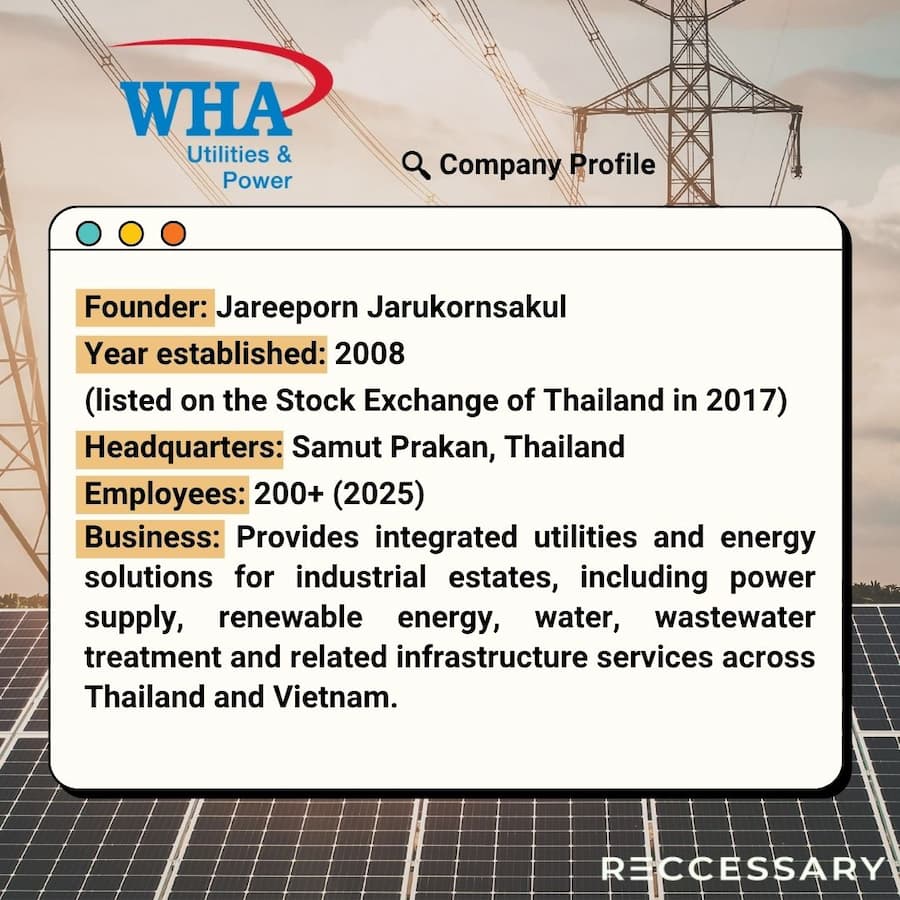

Thailand-based WHA Utilities and Power, part of industrial developer WHA Group, operates across both Thailand and Vietnam, providing utilities and energy services to tenants in its industrial estates. The company, listed on the Stock Exchange of Thailand (SET), has around 1 GW of operating capacity, including roughly 500 MW of renewable energy, primarily from solar. WHA also owns more than one-third of the 26 industrial estates in Thailand’s Eastern Economic Corridor, a key investment zone that has attracted billions of dollars from multinational companies.

Unlike standalone renewable developers, WHAUP positions itself as an integrated infrastructure provider, offering not only electricity but also water, waste treatment and digital services. Its client base spans a wide range of industries, from global technology companies such as Google operating data centers in Thailand to electronics manufacturers such as Foxconn in Vietnam, reflecting the diverse energy and infrastructure needs across markets.

WHAUP’s role extends beyond supplying utilities to individual tenants. As a developer and operator of industrial estates, the company is involved at an earlier stage of project planning, shaping how energy and other infrastructure are designed and deployed across entire industrial zones. This allows it to align power supply, water management and land development with the needs of incoming tenants, particularly those with large and complex energy requirements.

WHAUP positions itself as an integrated infrastructure provider, offering not only electricity but also water, waste treatment and digital services. (Photo: WHAUP)

“When we talk about data centers, it is not only about power. Water is also a key consideration,” Akarin said, adding that WHAUP aims to act as a “total solution provider” for its tenants.

WHAUP’s footprint in both Thailand and Vietnam highlights how manufacturing strategies differ across the two markets. Akarin said Thailand is focused on attracting high-tech industries such as data centers and electric vehicles (EV) ecosystems, while Vietnam offers strong potential for electronics clusters, supported by lower labor costs and good connectivity.

These differences translate into different expectations for energy. In Thailand, data center operators prioritize supply reliability first, with renewable energy targets remaining flexible until stable power supply can be secured. Over time, however, they are expected to ramp up renewable sourcing to meet long-term RE100 commitments.

In Vietnam, manufacturers are often more cost-sensitive but are increasingly incorporating renewable energy to meet export and supply chain requirements, said Akarin. To support this shift, WHAUP is expanding its private PPA portfolio, targeting an additional 29 MW of capacity in Vietnam, while positioning itself to capture future demand from direct PPA schemes, which are expected to exceed 2 GW as the market develops.

Rising demand meets structural constraints

Demand for renewable energy is increasing across industries, but not at the same pace. Akarin noted that every sector is asking for green power, with data centers having the most immediate requirements, driven by internal decarbonization targets. Electronics manufacturers and garment producers are also showing growing interest, particularly as renewable energy affects their ability to secure orders from global buyers.

From an industrial estate developer’s perspective, this shift is becoming more visible in how tenants define their energy requirements. “Every sector is asking for green power,” Akarin said, with demand increasingly shaping site selection decisions.

In response to this growing demand, WHAUP is expanding its renewable energy footprint in Vietnam. The company established WHA Solar Vietnam in January, with Akarin noting that the subsidiary had been part of its expansion plans for some time but was only set up after the permit was secured.

However, this expansion alone does not resolve the broader supply challenge. Current renewable energy solutions are still limited in scale, particularly within industrial estates. Most rely on rooftop solar, which can offer electricity at prices competitive with the grid, but is constrained by available space and sunlight hours. As a result, Akarin said rooftop solar typically covers only 15 to 20% of total power demand, leaving the remaining 80 to 85% dependent on grid electricity or other sources.

Akarin Prathuangsit, CEO of WHA Utilities and Power Public Company Limited. (Photo: WHAUP)

Akarin Prathuangsit, CEO of WHA Utilities and Power Public Company Limited. (Photo: WHAUP)

Policy frameworks opening new procurement pathways

Policy developments in both Thailand and Vietnam are beginning to open new pathways for renewable energy procurement, but implementation remains uneven. In Thailand, WHAUP is closely watching the upcoming pilot direct power purchase agreement (DPPA) scheme, which has an initial capacity of 2GW and is expected to target large electricity users such as data centers. “Once regulators are comfortable, the program could be expanded,” Akarin said.

In Vietnam, virtual DPPAs have been introduced, allowing companies to procure renewable energy through financial settlement mechanisms. While this expands access, Akarin said challenges remain around pricing uncertainty and investor confidence. He pointed to past cases where projects that had already reached commercial operation were subject to lower-than-expected tariffs, raising concerns over the stability of returns. As a result, developers are increasingly looking toward private offtake through DPPA structures.

At the same time, renewable energy intermittency requires additional system support to maintain grid stability. Declining battery costs are beginning to shift the economics of renewable energy in industrial settings. Battery systems can currently extend renewable energy use by two to three hours, and up to 24 hours depending on tariff arrangements with customers, helping companies reduce reliance on grid power and manage variability.

“In the past, there was little interest because battery costs were too high. But since the beginning of this year, we are seeing increasing inquiries,” Akarin said.

The recent rise in battery interest is not driven by cost declines alone. In Vietnam, new regulatory changes are beginning to reshape the economics of storage. A recently introduced two-part tariff structure allows battery systems to be compensated not only for the electricity they discharge, but also for their availability to support the grid. This creates a more stable and predictable revenue stream, improving project bankability and making storage more attractive to investors.

Looking further ahead, WHAUP is also exploring emerging technologies such as small modular reactors (SMRs), which Akarin described as a “game changer” that could provide stable, low-carbon electricity at scale.

Reliability and infrastructure shaping investment decisions

Differences in energy systems between Thailand and Vietnam continue to shape how developers and manufacturers approach investment decisions. Thailand benefits from a more diversified energy mix and stronger grid reliability, supported by multiple generation sources, Akarin said. Vietnam, while offering strong growth potential, faces greater challenges in terms of grid stability, he added.

For developers operating across both markets, these dynamics influence how projects are structured and how energy solutions are delivered to industrial customers.

“We are closely watching these developments and keeping pace with the technology,” Akarin said.

'Vietnam vs. Thailand competitiveness' series

- Energy as a competitive lever: How Vietnam, Thailand compete for green manufacturing investment

- Energy as a competitive lever: How GreenYellow is building renewable energy solutions for manufacturers in Vietnam

- Energy as a competitive lever: WHAUP integrates green power and infrastructure for industrial growth

- Energy as a competitive lever: CCET navigates renewable opportunities and constraints in Thailand

- Why Vietnam’s rapid rise and Thailand’s slower growth tell different investment stories

- How Thailand and Vietnam’s power reforms will reshape corporate energy strategy

- Execution over incentives: Thailand and Vietnam’s structural investment shift

RECCESSARY’s upcoming webinar, “Beyond ASEAN: Mastering Decarbonization Strategy in Thailand & Vietnam,” will take place on April 21.

The session will unpack net-zero regulations, CBAM readiness, green power procurement strategies, and what lies ahead for low-carbon manufacturing across Vietnam and Thailand.

Seats are limited. Register now.